Capital Sourcing

Redetermination Season Brings Slight Improvement, But Capital Access Still Tight

By Gregory DL Morris, Special Correspondent

Oil prices have improved significantly this year on expectations that widespread vaccinations will bring the COVID-19 pandemic under control, global energy law firm Haynes and Boone noted in its semi-annual survey of the price ranges that banks use for reserve-based lending. The survey found that if expectations are met, near-term oil and gas prices should recover above the banks’ spring 2021 price decks.

However, the firm cautioned, the historical level of bankruptcies and significant loan losses during the past few years are still fresh in the memory of many bankers. So, while conditions are improving, borrowing bases probably will see only modest improvement during this redetermination season.

“Accordingly, it is not likely that producers will see material improvements in borrowing-base redeterminations this spring,” Haynes and Boone’s recently concluded “Spring 2021 Borrowing Base Redeterminations Survey” states. The expectation among producers and bankers, as reported by respondents, is mostly either no change or a 10% increase on average from last fall’s borrowing bases.

The average spring 2021 base case for natural gas is $0.07 higher than the banks’ price decks from last fall, according to Haynes and Boone. “Although an improvement, it is not so appreciably better that it would indicate improvement during this spring’s borrowing base redetermination season for gas-weighted producers. Actually, the banks’ price decks for gas prices track lower than last fall’s price decks were forecasting. Until gas demand improves, it does not appear that there will be any gas lift to borrowing base redeterminations.”

In its borrowing base survey, released about the same time, Haynes and Boone further found that “after difficult borrowing-base redetermination seasons in 2020, producers should expect the spring 2021 redetermination season to result in continued, or even very modestly improved, RBL credit availability.”

Hedging levels, which were already historically high, have gone even higher, the borrowing-base survey found. Price improvements in recent months have motivated both producers and their lenders to protect against the downside.

“The upstream oil and gas industry has settled into a new normal with respect to capital raising,” Haynes and Boone states. “Expectations regarding capital sources have stayed extremely consistent in the past three redetermination surveys. The most significant change is an increased used of debt from capital markets. Three oil and gas plays–the Permian, Eagle Ford/Austin Chalk, and the Haynesville–will attract the most capital during the next two years. Though baseline economics are the biggest driver, the political landscape is likely also a factor; plays that involve significant federal leasing have minimal interest.”

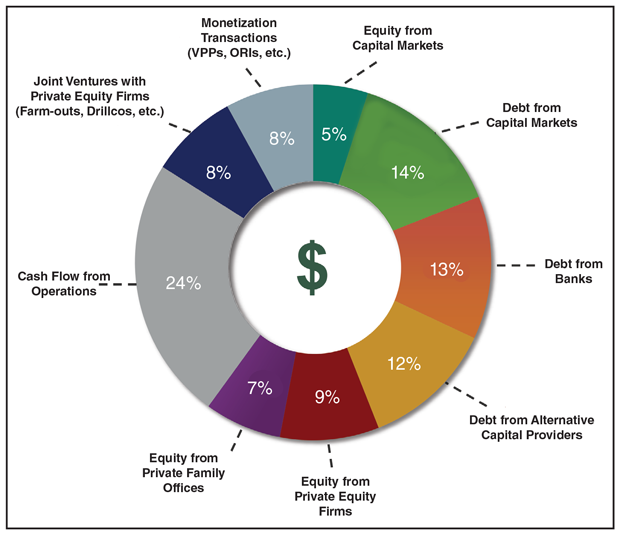

FIGURE 1

Producer Expectations for Capital Sourcing

Over Next 12 Months

Source: Haynes and Boone Spring 2021 Borrowing Base Redeterminations Study

Figure 1 shows producer expectations for capital sourcing options over the coming 12 months, according to results from the survey. Cash flows generated from operations was the most selected option, followed by debt from capital markets, debt from banks and debt from alternative lending sources. Respondents could select more than one option. A total of 444 responses were collected, according to Haynes and Boone, with the percentages representing the total responses for each respective option.

Other financial outlooks strike a similar tone. The improvement in the U.S. macro narrative has impacted the oil markets, according to the most recent ABN-Amro commodity review. “After a few weeks of sideways trading, oil prices rose based on lower U.S. crude inventories and higher demand expectations. Both OPEC and the International Energy Agency raised their demand expectations for 2021, especially for the second half of the year.”

ABN-Amro noted that the changes “come after OPEC+ decided to increase its oil production in the months May, June and July with a total of 1.15 million barrels a day. Also, Saudi Arabia will unwind its voluntary production cut of 1 MMbbl/d. As a result, a total of 2.15 MMbbl/d will be added to production by the end of July to balance the rise in demand.”

According to the report, ABN-Amro expects oil prices to trade around $60/bbl for the remainder of the year, further refining that forecast to an average of $62/bbl for Brent and $59/bbl for West Texas Intermediate.

For natural gas, the cold spell in early April triggered higher demand, which has resulted in below-average inventories. “The later end to winter weather will mean it will take longer to restock gas inventories, which will keep demand higher than normal during the coming weeks,” the ABN-Amro forecast said. “As a result, we have lifted our natural gas price forecasts for 2021.”

Reluctant To Lend

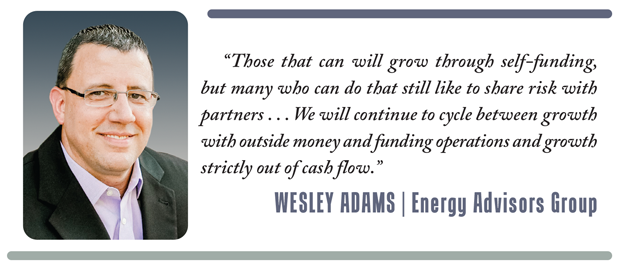

Even though semi-annual redeterminations were not harsh this spring, banks are clearly reluctant to lend, even for traditional reserve-based borrowing, observes Wesley Adams, director of acquisitions and divestiture firm Energy Advisors Group. The redeterminations were not severe, so banks seem to be coaxing their existing borrowers along. With public equity markets largely closed, there remain a few options for operators. “Those include friends, family offices, and mezzanine finance groups, as well as private equity groups and funds focused on yield,” he says.

As bleak as the capital picture may seem at present, bank lending is not lost forever for independent producers. “Banks will never go away because their capital is cheap compared with the alternatives,” Adams comments. “Every company has at least one bank, and often has close relationships with its bankers, especially when it banks locally or regionally. So, yes, banks will be able to win that business back if they want to, and the market is such that bank financing can provide what companies need.”

Public markets also remain open at least a crack. Late in March, Vine Energy announced that the underwriters of its previously announced initial public offering of 21.5 million shares of its Class A common stock fully exercised their option to purchase an additional 3.225 million shares at the IPO price of $14/share, less the underwriting discounts and commissions, resulting in additional net proceeds of approximately $43 million. Citigroup, Credit Suisse, Morgan Stanley, Barclays, BofA Securities and RBC Capital Markets acted as joint book-running managers for the offering.

As if an IPO of an upstream independent shale player was not rare enough, Vine is neither in the Permian nor oil-weighted. It produces mostly dry gas in the Haynesville and Middle Bossier plays.

As operators improve their economics and financial self-discipline, Adams notes that they will be able to fund more development on their own. That increasing self-sufficiency makes them a better risk. He reiterates the adage that every mortgage applicant knows: Banks tend to lend to those who can prove they do not need the money.

“I think those that can will grow through self-funding, but many who can do that still like to share risk with partners,” he remarks. “The focus right now is fiscal discipline. Wall Street is punishing growth and is focused on alternatives, so operators do not have much choice in the matter.”

Funding Cycles

Fiscal discipline by operators and attractive rates of return for the market will encourage public capital to take a fresh look at upstream independents, Adams suggests. “Public companies seem to be more sensitive to public perception, and therefore, make decisions many times based on public opinion rather than market fundamentals.”

Patience is the key virtue, Adams stresses. “There will always be funding cycles. Private equity will come back around if there are not as attractive alternative investments. Banks will only be useful to those that do not need the money, but want to borrow instead of spend their own capital unless sellers come down on their expectations,” he says. “We will continue to cycle between growth with outside money and funding operations and growth strictly out of cash flow. Companies cannot become impatient and try to grow faster than cash flow allows. Otherwise, they risk cycling back to trying to live on cash flow from operations.”

Private money–both equity and debt–remains a major source of both operating expenses and capital expenses for independents. There seems to be plenty of money, plenty of limited partners willing to invest and no reluctance by general partners or management firms to lather, rinse and repeat with experienced management teams, according to Adams.

“Teams that have made significant money for their backers tend to get taken care of until either the money tires of the space, the management team dissolves or it just cannot find any good projects,” Adams says. “I think that capital realizes that oil and gas is not going to be replaced any time soon, so providers want to be ready to act when the next price spike occurs or when a downturn occurs and they can buy assets cheaper.”

Reviewing alternative forms of funding, Adams indicates “there is a lot of activity in the nonoperated arena, especially in drilling in the Midland and Delaware basins, as well as some in the Haynesville.”

In contrast, he adds that the issue with mezzanine financing is that the projects have to have enough margin to accommodate the cost of capital. “Structured deals like volumetric production payments, term overrides, and other arrangements are being discussed. Trading workover capital for working interest is also popping up.”

Energy Advisors Group is on a buy-side retainer for a group with funds for that purpose. “I am constantly on the lookout for new types of capital,” Adams says, “but the Achilles’ heel always seems to be a lack of equity provided by the management team to satisfy the lenders. The biggest key to getting funded is having money in the form of cash or existing production.

“I am not seeing much capital available to pay overhead for new teams with no assets and no cash to put into the projects they want to do,” he continues. “The lone exception is those willing to fund workovers to get that production, but that even requires having an asset to workover.”

Select Transactions

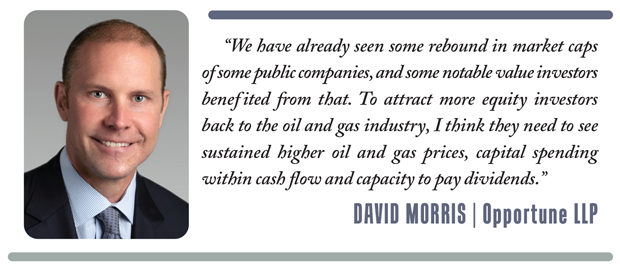

Across the industry, independent companies are finding capital harder to come by, relates David Morris, managing director of Opportune LLP’s restructuring practice based in Dallas. “I think all lenders and investors in the oil and gas industry have become more selective about the new transactions they fund,” he comments. “It is not just the commercial banks. This observation seems consistent with the responses in Haynes and Boone’s spring 2021 survey.”

In terms of sources of capital, Morris notes, respondents to the survey indicated that operating cash flow would be the primary source of capital (24%). That was followed by debt from capital markets (14%), banks (13%) and alternative lenders (12%). “We have seen significant bond issuances in the first quarter of 2021, but there are many companies that cannot access the high-yield market,” Morris adds.

For all the hesitancy in lending, RBL options provided by commercial banks remain the least expensive source of capital for upstream independents, Morris states. “It is hard to imagine that executives will forego that capital if it is available for their companies. Therefore, I expect those companies that have refinanced debt with higher-priced loans from alternative lenders during this downturn to return to the RBL market as soon as possible.”

In that same spirit, he adds that becoming self-sufficient by funding capital expenditures with operating cash flow is a common goal for producers today. “However, I do not foresee an end to debt financing for growth-driven deficit spending,” Morris observes. “That being said, the hurdles to raise capital for growth investments are certainly higher today.”

Private equity remains available for executive teams with strong track records, Morris goes on. “I think there is a lot of money available for experienced, successful management teams to buy top-tier assets at discounted prices, but those deals are few and far between today. Limited partners and general partners are proceeding more carefully now as the lather-rinse-repeat strategy has been undermined by several factors that have disrupted their typical exit strategies into the A&D and IPO markets.”

Morris says he even sees some cause for optimism in the public markets. “We already have seen some rebound in market caps of some public companies, and some notable value investors benefited from that,” he remarks. “To attract more equity investors back to the oil and gas industry, I think they need to see sustained higher oil and gas prices, capital spending within cash flow and capacity to pay dividends.”

At the same time, he says, “There has been a noticeable increase in alternative lenders such as credit funds, family offices and so forth, engaging in and responding to upstream companies’ financing processes over the last six months or more,” Morris explains. “However, those lenders remain very disciplined about the deals they ultimately pursue, favoring plays with the strongest economics.”

Alternative capital continues to show interest in various financing options to fund debt repayment, CAPEX and acquisitions, including uni-tranche loans to replace traditional RBLs, volumetric production payments (VPP), sales of overriding royalty interests (ORRI), and drillco joint ventures with and without reversions, Morris details. Antero Resources, for example, closed a $402 million ORRI transaction with Sixth Street Partners last June and a $220 million VPP with an affiliate of J.P. Morgan in August.

Those kinds of financial tools continue to grow in importance, Morris suggests. “Companies, investors and alternative lenders should continue to monitor the traditional RBL market. Several commercial banks have exited or are in the process of exiting the RBL business, and some others that may remain are still focused on reducing exposure to oil and gas companies. As a result of those factors and others, new RBLs are expected to be smaller in general, which may continue to drive activity to alternative capital sources.”

Perfect Storm

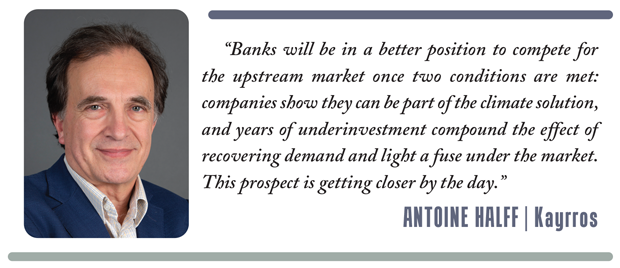

Antoine Halff, co-founder and chief analyst at data analytics firm Kayrros, says a perfect storm is driving the banks away from funding upstream independent companies. “First is poor returns amid weak oil demand in the wake of COVID-19. Second is climate policies and their negative impact on public perception of the sector’s longer-term viability,” he lists. “Last is growing pressure on the banks themselves to go green and abandon fossil fuels.”

In contrast, Halff notes that private money is “inherently less sensitive to environmental, social, and governance factors, less interested in displays of sustainability and more willing to back up oil ventures. The more banks limit the oil sector’s access to capital, the more opportunity it creates for private money, both by opening up market share and by raising the odds of another supercycle due to underinvestment.”

Which is not to say that bank lending is done for good. “Not at all,” Halff responds. “Banks will be in a better position to compete for the upstream market once two conditions are met: companies show they can be part of the climate solution, and years of underinvestment compound the effect of recovering demand and light a fuse under the market. This prospect is getting closer by the day.”

Recent activity in mergers and acquisitions has transformed the U.S oil patch, Halff notes, “leaving a small group of international oil companies and oversized independents in control of a much larger share of what had been a highly fragmented sector. This new big oil club is more disciplined, more focused on return on investment and more inclined to fund operations themselves from their balance sheets. But some of those companies had to take on debt to expand.”

Among the more sanguine analysts, Halff’s outlook is positive. “ESG concerns aside, there are good reasons to believe the oil sector has been severely undervalued and sits on the cusp of a big correction,” he offers. “Those include a looming supply shortfall as well as recent remote-sensing technology breakthroughs that are empowering companies to not only slash greenhouse gas emissions at scale, but also communicate effectively about it in a transparent and verifiable way. That is not lost on private money.”

The key factor will be the decarbonization of the oil and gas supply chain, he suggests. “Right now, the sector is under a cloud and considered a climate villain,” Halff concludes. “The irony is that oil and gas companies, for the first time, are in a position to cut emissions at scale, at speed and at little cost.

“Kayrros Methane Watch technology shows that oil and gas production accounts for 64% of anthropogenic methane “hot spots” worldwide, even more than previously thought. The good news is the same technology that makes those leaks visible also makes them avoidable, enabling companies to prove their progress in eliminating them,” he continues. “Once that happens, it will make a strong case for investing in climate-friendly operators.”

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.