Tuscaloosa Update

Tuscaloosa Marine Shale Rewards Persistent Independents

By Gregory DL Morris, Special Correspondent

After a flurry of activity in the Tuscaloosa Marine Shale (TMS) met with some unexpected geological challenges three years ago, the persistent independent producers that stuck with the play say they are being rewarded for their tenacity. Sprawling across 2.7 million acres of southern Louisiana and Mississippi, they say the TMS is a well-documented but largely unproduced oil play estimated to contain nearly 7 billion barrels of recoverable resource.

A significant vote of confidence came in June when private-equity investor Apollo Global Management backed Halcón Resources in the TMS with an initial investment of $150 million toward a possible total of $400 million. Halcón is one of the three top acreage holders, along with Goodrich Petroleum and Encana Corporation. There are also a few smaller players active.

According to reports, acreage is modest by the standards of other shale basins, ranging from $700 to $4,500 an acre, but well costs put the play at the top of the national range.

Financial Joint Venture

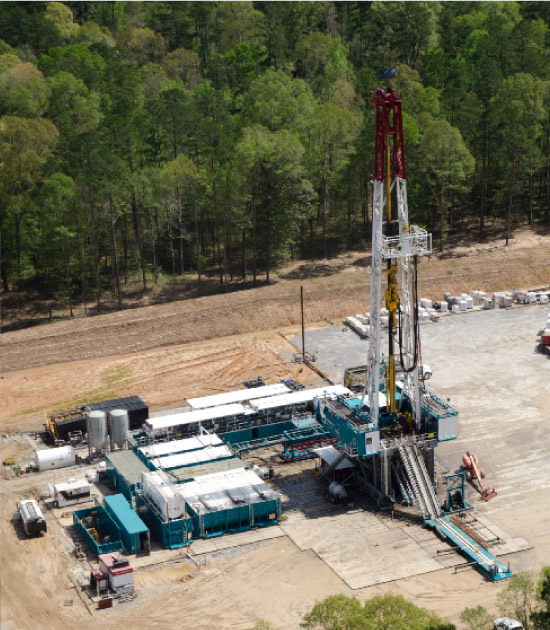

Halcón has about 320,000 net acres leased or under contract in Louisiana and Mississippi that the company says it believes are prospective for the TMS. Halcón got into the eastern part of the TMS in autumn 2013 and quickly put together 200,000 acres, says President Stephen W. Herod.

With its land position secure, Herod says, “We considered the best ways to finance development within our capital structure and financing. We decided to explore a joint venture, and started talking to people late last year. There was lots of interest because of our track record in shale development, going back to Petrohawk Energy Corp., and because the TMS was starting to catch fire.”

The discussions with Apollo came to terms in May and the deal was closed in June. “They are an excellent group,” praises Herod. “They have a great deal of familiarity with the industry and a significant amount of capital.”

Herod details some of the motivation behind the unusual structure of the investment. “We did not want to sell down any of our position,” he explains. “Typically, operators sell 20-30 percent of their interest in return for a cash-and-carry combination. We did not want to give up ownership or control of our acreage or our wells. So we arranged a financial joint venture where Apollo provides capital to a subsidiary that holds the acreage. It gets a return through a coupon payment and an override on some wells, but we retain 100 percent of the acreage.”

Importantly, he adds, the terms are nonrecourse to the parent company. After the initial $150 million investment, Apollo will have to make a decision next year about increasing its stake to the maximum $400 million. “We and they are evaluating the development so far,” says Herod.

The Apollo investment is not a conventional arrangement, Herod allows. Rather, Apollo will invest in Halcón’s wholly owned subsidiary, HK TMS LLC, which will own all of Halcón’s acreage in Mississippi and Louisiana that is prospective for the TMS. Halcón retains 100 percent of the HK TMS common shares and is the sole manager. Herod says Apollo initially paid $150 million cash for 150,000 HK TMS preferred shares, and can buy another 250,000 preferred shares on the same terms. Holders of the HK TMS preferred shares will receive quarterly cash dividends totaling 8 percent a year.

Also, Herod points out, HK TMS assigned a 4 percent overriding royalty interest–subject to a reduction to 2 percent under certain circumstances–in 75 net wells. The number of wells in the royalty structure will increase as Apollo acquires preferred shares up to 200 net wells.

Reservoir Quality

Halcón reports its first well, the Horseshoe Hill 11-22H-1 (92 percent working interest) in Wilkinson County, Ms., achieved a 24-hour average initial production rate of 1,208 barrels of oil and 1.1 million cubic feet of 1,551 Btu gas on a 19⁄64-inch choke. Based on gas composition analysis and assuming full ethane recovery, the company estimates the well could produce an additional 212 barrels of natural gas liquids a day for a total 24-hour average initial production rate of 1,548 barrels of oil equivalent.

The well has a 7,060-foot effective lateral and was completed with 24 fracture stages, 21 of which Halcón says were pumped effectively and three of which were pumped partially because less proppant was placed than designed. Halcón drilled the well in 39 days.

Halcón subsequently completed three more wells over the summer, and says it plans to spud a total of 10-12 operated wells in the TMS this year, running an average of two rigs through the end of this year. The company says it also expects to participate in 15-20 nonoperated TMS wells this year.

Executive Vice President and Chief Operating Officer Charles E. Cusack III says it was the quality of the reservoir that attracted Halcón initially. “We had countless maps and a great deal of geological work. We realized the TMS was a world-class reservoir,” he says. “Most of the details have been published, so it is easy to see how we came to that conclusion.”

Such enthusiasm begs the question of why such a purported gem is only now being developed. “What put the ding on the play,” Cusack relates, “was that there were more bad wells than good ones when drilling started.”

But rather than being scared off, he says Halcón dug into the forensics. “Ultimately, we were able to understand why just about every well went bad,” Cusack reports. “There were short laterals and understimulated completions. Sometimes there was not enough proppant. There was a lot of trial and error with slickwater, which does not work in this play. Some perforation clusters were spaced too widely, and sometimes the wellbore just landed out of zone.”

Based on those findings, Cusack says the keys to the TMS are becoming clear: a large completion design with a lot of fluid and a lot of proppant. “The top three operators–Encana, Goodrich and us–all are gravitating to similar techniques,” he advises.

Herod says that Halcón plans to continue running two rigs through the end of the year, and hopes to increase that count in 2015, as are the other major players. Long-term, he says the business model is clear.

“Look at our history. Floyd Wilson (chairman and chief executive officer of Halcón) built several companies and eventually sold them, such as Petrohawk. So ultimately, we expect to merge or sell Halcón, but we don’t know when that will be, so we build and operate as if we are going to continue operating. Once we can derisk a lot of locations, at some point that is likely to be desirable to a larger company.”

Cusack confirms, “We are staffed and capable of fully developing and operating in the TMS for the long term.”

Goodrich Petroleum is running three rigs in the Tuscaloosa Marine Shale, drilling seven to eight wells per rig per year. President Robert C. Turnham reports the company has zeroed in on 5,000- to 8,000-foot laterals as optimum, and pumps 450,000- 550,000 pounds of proppant per fracture stage.

Land Office Business

Of the 50 wells producing in the Tuscaloosa Marine Shale, Goodrich Petroleum owns 20 of them. The company has in excess of 300,000 net acres, and with three rigs running, is completing a new well roughly every 15 days.

President Robert C. Turnham says his firm’s three rigs are spreading wells around the block. “There is very little variability and lots of natural fractures, so we are finding that wells produce at high rates initially from a combination of natural and frac-induced fractures. The decline curves are very similar to other shale plays,” he reveals. “We plan to increase our rig count to as many as five, and are seeking new partners. We are running a soft process to find interest, and Sinopec Limited is involved. We hope to have something in place before the holidays, and then hope to have as many as eight rigs running next year.”

Goodrich has been able to drill seven to eight wells per rig per year, and has driven down spud-to-sales time from 75 to 60 days. The plan calls for pad drilling to begin next year for at least two rigs. “The big question is scheduling the fracturing jobs,” Turnham says. “We work with Halliburton, and it has been very responsive.”

The good news for those on the outside looking in is that small tracts of land still are available in the TMS. “In the long run, we may sell some in the Eagle Ford, once we get further in the TMS,” Turnham states. “This play is a company maker for us, but for now, we have more acres in the TMS than we can say grace over.”

That said, he reports, “The market is still reasonable. Land is going for up to $4,500 an acre with a 20-25 percent royalty. The catch is that there are not any big tracts left.”

In late September, Goodrich reported that its Bates 25-24H-1 well (98 percent working interest) in Amite County, Ms., achieved a 24-hour average production rate of 1,000 boe, consisting of 983 barrels of oil and 373 Mcf of natural gas. The well was completed with a 4,850-foot lateral and stimulated with a 19-stage fracture.

In addition, the company’s CMR/Foster Creek 31-22H-1 (90 percent working interest), in Wilkinson County, peaked at 1,140 boe/d during the early stages of flow back on a 13⁄64-inch choke. The 6,700-foot lateral was fractured with 24 stages.

Goodrich also was in the completion phase on a second Wilkinson County well (97 percent working interest)–the CMR/Foster Creek 24-13H-1–in September, Turnham reports, as well as the Spears 31-6H-1 (77 percent working interest) in Amite County, and the Verberne 5H-1 (66 percent working interest) in Tangipahoa Parish, La.

“We bought our initial TMS acreage two and a half years ago,” recalls Turnham. “We were able to aggregate positions from speculators or from operators who had been working shallow. The original position was 135,000 acres. We were monitoring Devon Energy, which was the first mover. We bought out Devon a year and a half ago, and that added 180,000 acres. We studied the log and core data, and found no material difference between our rocks and Devon’s.”

Driving Down Costs

Turnham says the completion recipe used in some of the early Tuscaloosa Marine Shale wells was very different from what Goodrich uses today. “In the early days, operators were using 90,000-300,000 pounds of proppant per fracture stage. We are using 450,000-550,000 pounds,” he reports. “It is a very complex fracture network and we are using a combination of techniques to transport the proppant into the fractures.”

Part of the challenge, he adds, is that the TMS is overpressured and very rich. “The hydrocarbons in place are 92-96 percent oil, and you have to stimulate them. Big frac jobs do that much better,” Turnham outlines. “Also, some of the early intervals were too wide–300 feet or more. We have found that 250-270 feet are better. In general, bigger, tighter and longer laterals are better. Some early laterals were 3,000-3,500 feet; we are now going 5,000-8,000 feet.”

When Goodrich acquired Devon’s position, it acquired Sinopec as a partner. “It is a ground-floor, one-third partner,” says Turnham. “There are 90,000 acres in which Sinopec has a working interest from which it is taking its share of revenue. It is a typical nonoperator interest. We allow Sinopec two engineers in our Houston office to share information, but we also teach them. The partnership is going very well.”

The TMS certainly has its tricks, Turnham continues. “It is a complicated area that is overpressured,” he characterizes. “The rubble zone is a big positive, once a well has been completed and you are into development, but drilling has been a challenge for operators. We got through it at a steeper pitch, which solved some of the sloughing problems. We also kept away from landing higher in the horizon. That brought us into a softer clay zone that resulted in some pipe crimping, but we have been able to eliminate that, for the most part. The play certainly has presented its completion challenges, but they are largely behind us.”

He adds that Goodrich has been able to reduce drilling time from 45 days for the first few wells to 40 and even 25-35 days in a few cases. “Driving well costs down is very important,” he remarks. “Every drilling day is $100,000.”

Once the resource is brought to the surface, “TMS crude is light and sweet. It is 38-42 gravity crude that gets a premium price,” he describes, noting that in September, Louisiana Light Sweet was receiving a $4 premium over West Texas Intermediate.

Turning to the question of why the TMS is only now being developed, Turnham reasons, “Everyone knew there was oil in the 10,000-15,000-foot ranges, and that the deeper horizons had higher pressure. There was shallow production already, and that had to be protected until drilling and fracture techniques could be developed.”

He says he is optimistic well costs can be brought lower. “We knocked $3.5 million off Eagle Ford wells from the start of development to where we are now,” he points out.

Encana Corporation has two rigs operating in the Tuscaloosa Marine Shale and hopes to complete between nine and 12 wells before the end of the year. Executive Vice President of Exploration and Business Development David Hill describes the TMS as deep, high pressure and high temperature. He says issues such as well integrity and mud density have been challenges, but that operators are homing in on best drilling and completion practices, including cluster spacing, perforations per cluster, and the amount of proppant and fracture fluid per stage.

Working In A Tight Window

Encana has two rigs operating in the Tuscaloosa Marine Shale and hopes to have between nine and 12 wells completed by the end of the year on its 200,000-acre block. “The key is the repeatability of the type curve,” offers David Hill, executive vice president of exploration and business development.

He says a complete appraisal of the TMS is due by the end of the year, with a full development plan to follow soon after.

“This play is deep, it is high pressure, and it is high temperature,” Hill states. “Tripping adds time and complications, as well as being a strain on borehole stability. Operators have had to overcome challenges to well integrity and mud optimization, especially mud density. But we are homing in on a good design from drilling to completion, including cluster spacing and perforations per cluster, and also amount of proppant and fluid per fracture stage. There is a very tight window in this play, but this is what we do for a living.”

Cooperation among operators generally is cordial, but can be a bit frosty in some plays, Hill observes. In contrast, he says the TMS is a mutual-aid society. “This play very much depends on all the operators to progress,” he poses. “Each play takes on its own identity, which has something to do with the number of players. Where there are more (companies active), there usually is less sharing. There is also a Schlumberger consortium in the TMS that is working to address technical issues. All the major operators are in it.”

Hill emphasizes the geological challenge of the Tuscaloosa Marine Shale. “The key is being disciplined, monitoring our wells, and monitoring our peers and their wells,” he says. “It is very important to see well data and lateral length. Designed lengths are getting out 7,000 feet.”

Checking The Boxes

Kirk Barrell, president of Amelia Resources, confirms the TMS is all hands to the wheel. “It is easier to make friends when you are all struggling,” he jokes. “After watching Devon stumble, the rest of us really pulled together. Also, there is a lot of overlap in acreage, so it is easier to cooperate and swap to secure a better position. In the TMS, there has been more sharing of information than I have ever seen.”

Amelia is not an operator, but assembles drilling packages and retains an overriding royalty. Deals to date have covered 128,000 acres. “I have been active in the TMS for 23 years, going back to my Amoco days,” Barrell reveals. “This play developed much later than other shales because it is much deeper. The TMS today is comparable to the Eagle Ford Shale in 2009. Wall Street has been hard on producers in the play because Wall Street wants the TMS to be like the Eagle Ford in 2014.”

Barrell explains that operators have had to overcome the challenge of discovering the correct angle at which to approach their landing, and to get comfortable with the most effective completion techniques. He says they have checked all the boxes but one: cost. Wells cost around $14 million, which Barrell says makes the TMS probably the most expensive unconventional play.

However, initial production rates are very good, as are decline curves, he goes on, “so the future is going to be all about repeatability. That will help bring costs down.”

Barrell comments that “compared with land costs in the Utica or the Permian, which are running $8,000 an acre, the TMS is $700 to $2,000 an acre.”

And that is not for marginal property only. “I don’t like the terms ‘core’ or ‘sweet spot,’ but within the economic limits of the TMS, there are acres still available,” Barrell insists. “Of course, the comfort level is to the center, but there are good data and good acreage available. Well costs have scared off some people, especially private equity, but given the entry costs versus the upside, I am shocked that other players have not shown up sooner.”

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.