Innovations Poised To Improve Economics of Second-Tier Acreage

Except for the Permian and Appalachia, most U.S. shale basins will run out of Tier I acreage in less than four years, according to a report by McKinsy & Co. In this context, McKinsey classifies acreage as Tier 1 if its oil production breaks even below $40 and its gas production breaks even below $2.30 per million Btu.

“Tier 1 drilling locations—those with the best geology—are running out,” the firm says. “Yet a vast Tier 2-plus inventory remains and could potentially sustain operations for more than 15 years across most basins, if operators can successfully enhance the economics of these locations.”

Several paths to achieving that goal exist. “We have identified 27 emerging innovations that could reduce both capital and operating costs, and even unlock higher recovery factors, reducing breakevens by between $7 and $13 per barrel of oil equivalent,” McKinsey says. “These innovations could elevate between 55,000 and 80,000 Tier 2 drilling sites to Tier 1 status, potentially extending shale’s peak by up to three years and increasing U.S. onshore oil production to as many as 13 million barrels of oil per day.”

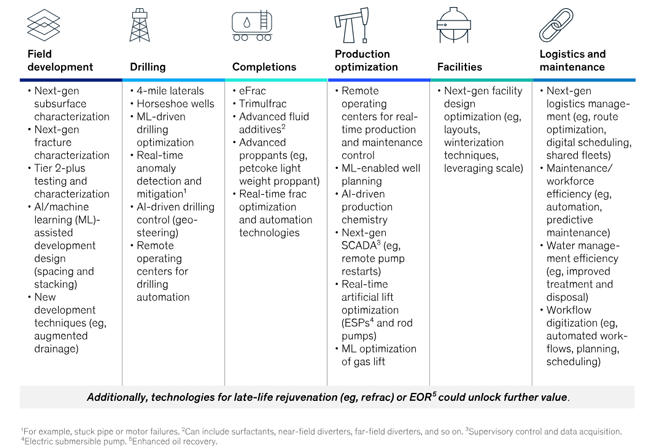

Figure 1 lists the 27 innovations. “Many of these innovations focus on expanding the boundaries of current methods,” McKinsey notes. “Lateral lengths, for example, have risen from two to three miles on average, to four miles—setting a new standard when lease boundary constraints allow, and with horseshoe wells and other creative designs becoming increasingly common.”

FIGURE 1

A Non-Exhaustive List of Technologies and Techniques that are Pushing the Envelope

Source: McKinsey & Co.

Other innovations involve emerging technologies that could have tremendous benefits if they scale. As examples, McKinsey offers next-generation characterization and advanced logistics management.

“Then there are the potential “moonshot” innovations—those that could meaningfully enhance recovery factors—such as advanced lightweight proppants,” the firm continues. “If proven effective and scalable, these have the potential to extend shale’s peak and redefine the boundaries of what is possible in the industry.”

According to McKinsey, the cost savings and recovery increases these innovations deliver could cause breakeven prices in most basins to fall 17%-32% over the next five to 10 years. “While these figures may seem ambitious, breakevens from 2014 to 2017 dropped by 30% to 40% across shale, demonstrating what can be achieved,” McKinsey says.

Impact on Activity

Lower breakevens will cause operators to increase activity, McKinsey predicts. “The impact on capital deployment in the United States could be substantial,” the firm writes. “More than 700 additional wells could be drilled per year compared to our current outlook, despite total capital expenditure dropping as costs come down.

“The distribution of additional activity across basins would vary widely,” it says. “The Permian Basin, with its already extensive Tier 1 inventory, would likely see the smallest proportional impact over the next ten years. Other basins show potential increases of 10% to 20% in well counts as their large Tier 2 banks become more economical.”

Already-strong acreage would still benefit from the innovations. “Across basins, the Tier 1 profitability index for new wells could increase by over 20%, from an average of 1.8 to 2.3 as breakevens reduce,” McKinsey details. “These returns would be amplified in large, consolidated oil basins, with Permian leading the way. While Appalachia could see cost reduction benefits, the returns impact would be lower than other basins due to continuing midstream constraints that would limit new drilling over the next decade.”

McKinsey says lower breakevens in oil plays could dampen activity in dry gas plays by increasing associated gas production. It envisions some gas production shifting from the Haynesville, Eagle Ford and Mid-Continent to the Permian.

Collectively, McKinsey says the 27 innovations could increase free cash flow by $40 billion to $70 billion over the next 10 years.

“However, increased production levels are never static—they require additional breakthroughs and activity to sustain them, putting an ever-increasing premium on R&D, underpinned by rigorous execution in the field,” the firm says. “Cash returns to shareholders therefore must be balanced against R&D and technology investment to drive productivity gains.”

The full report, Shale’s Next Surge: How 27 Innovations Could Unlock a New Growth Era, discusses the innovations’ implications for oil field service companies, midstream firms, petrochemical suppliers and refineries. It includes a graph that divides some of the innovations into three categories: proven, emerging, and breakthrough.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.