Range Of Opportunities Driving Williston Basin Activity For Operators Of All Sizes

By Danny Boyd

The Williston Basin of western North Dakota and eastern Montana is the classic “shale play curve” archetype. Prior to 2008, the basin was considered mature and production was on a gradual decline slope. But then the horizontal Bakken Shale play sprung to life, fueling one of the most legendary growth cycles in the history of an industry full of legendary booms. Daily oil production skyrocketed from 250,000 barrels in 2008 to more than 1 million barrels by 2014.

After topping 1.4 million bbl/d in 2019, the year-over-year growth during the Bakken’s first decade has transformed into a steady, stable trendline over the past four years that has maintained Williston oil output around 1.25 million bbl/d on average. The name of the game in the basin today is longer laterals, improved completion performance, optimized pad operations, and increasingly, extending Bakken/Three Forks development into untapped acreage outside the traditional boundaries of the geologic core.

Expansion of three- and four-mile drilling inventory continues while completion techniques boost yields from new wells and refractured legacy assets. The outcome is driving success for players across assets classes, including operators Formentera, Chord Energy and True Oil, non-operator Vitesse Energy, and royalty minerals buyer Mesa Minerals Partners.

Bakken Oil And Gas

Despite its oily history, the Williston is becoming gassier, again following prototypical tight oil development expectations. More gas means a greater need for more takeaway capacity with WBI Energy considering the Bakken East Pipeline to supply regional markets.

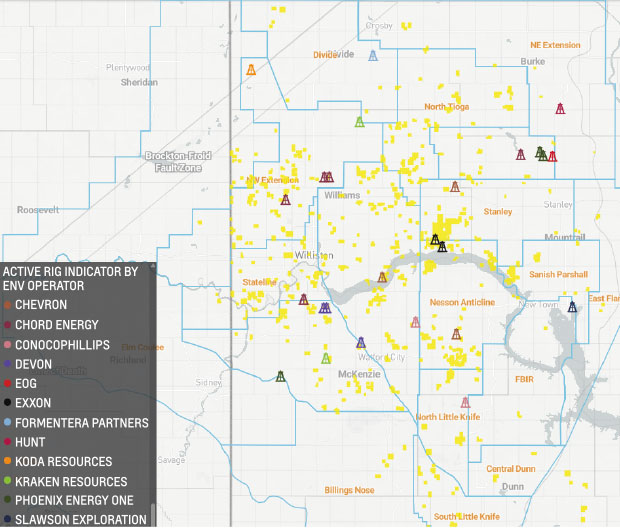

Formentera Partners and its operations arm, Formentera Operations, are extending the Williston core farther north across a 170,000-acre position built from three acquisitions over five years in Divide and Burke counties, N.D.

Formentera Partners is elevating to Tier 1 status much of a less-drilled northern portion of the Williston Basin on its 170,000-acre position in Divide and Burke counties, N.D. With more than 10 years of three- and four-mile horizontal drilling inventory, Formentera has one rig drilling about two Middle Bakken/Three Forks wells each month that are then completed with 1,000-1,500 pounds of proppant per lateral foot.

Technology supporting longer laterals and innovative completions at lower costs is quickly elevating to Tier 1 status much of a less-drilled northern portion of the basin bordering Canada, says Managing Partner Blake London.

“The world is starting to wake up to the fact that the northern part of North Dakota is competitive economically within the United States and globally,” he relates. “With laterals getting longer, efficiencies are only going to get better.”

Formentera has more than a decade of drilling inventory consisting mostly of three- and four-mile horizontals with no need currently to drill creative laterals. To prepare for development ahead, all its North Dakota properties were recapitalized last year after Formentera and a partner, Liberty Resources, improved development economics with their first three-miler in 2023.

Formentera has one rig drilling about two wells monthly into the Middle Bakken and Three Forks, completed with 1,000-1,500 pounds of proppant per lateral foot. Pads are typically designed with four wells, according to London.

London co-founded the Austin, Tx.-based company in 2020 with Bryan Sheffield as a private equity firm focusing solely on Formentera Operations instead of spreading capital among multiple portfolio companies. Separate funds for managing drilling and proved, developed, and producing assets were eventually merged because of significant investor overlap.

In 2008, Sheffield founded Parsley Energy, later acquired by Pioneer Natural Resources headed by Bryan’s father, Scott Sheffield, prior to Pioneer’s 2024 sale to Exxon Mobil. The younger Sheffield teamed with London after the two worked closely on Parsley’s 2014 initial public offering, which London oversaw as head of energy equity capital markets at Credit Suisse Group AG.

While some investors were shying away from oil and gas coming out of the pandemic, the partners saw an opportunity for a new kind of company that is operator, capital raiser and investor, London says. Partners Paul Treadwell and Stephanie Reed have since joined the company along with an experienced executive and operations team.

Formentera has raised about $3 billion since its inception to buy 800,000 acres in the Williston, Permian, Eagle Ford, Anadarko, Appalachia, the Barnett Shale, and on the Gulf Coast. Daily production is now approaching 70,000 boe/d, of which 60% is oil. Holdings also include 1.8 million acres in a shale play in northern Australia and potential in Venezuela after Bryan Sheffield attended President Trump’s White House gathering of energy executives following the capture of former Venezuelan President Nicolás Maduro.

Down the road, gas options will further enhance growth initiatives in the northern Williston, London says, but in the meantime, competition for oil assets continues to intensify amid mergers and entrances among private players that in recent years include Phoenix Energy, Koda Resources, Kraken Resources, Silver Hill, and others.

“A lot of people have assumed the Williston was kind of at its peak, but I think there is a second life in it, albeit we are having to quickly figure out who has the remaining opportunity available, but we are excited about it,” London remarks.

Crown Asset

The Williston’s Red Wing Creek Field in McKenzie County, N.D., is already True Oil’s crown asset, says Executive Partner Dave True. Several wells are on the table for drilling, along with prospects on other proven Williston acreage in eastern Montana pending a settling out in the markets from the Iran conflict.

“We are hopeful that oil prices will stabilize at a level that justifies that work and we can go forward with it,” True comments. “If we feel like prices are going to stabilize down at the mid- to upper $60s, that would be good. If they go much below that level, these assets will be saved for a later date.”

Based in Casper, Wy., True Oil discovered Red Wing in 1972 and later initiated a miscible hydrocarbon flood on the buried, Triassic-aged meteorite impact crater (or astrobleme) about 5.5 miles wide that includes a central uplift, a ring depression, and an outer rim.

Two Three Forks wells drilled with two-mile laterals over the past 18 months in the McKenzie County field are good producers, True says, and the company is eyeing a three-miler in the area.

Two slant holes have been drilled in the ring around the astrobleme. There are no further plans for development on the structure currently, but he explains that future ring drilling is possible.

True Oil is planning new drilling in its Red Wing Creek Field in McKenzie County, N.D., along with prospects on proven Williston acreage in eastern Montana. The company discovered Red Wing in 1972 and later initiated a miscible hydrocarbon flood on the buried, Triassic-aged meteorite impact crater, which measures 5.5 miles wide and includes a central uplift, a ring depression, and an outer rim. True Oil has recently drilled two Three Forks wells with two-mile laterals and is now planning a three-mile lateral.

While growth considerations are always on the table, there are fewer options to acquire assets as competition intensifies and technological advancement has translated into fewer divestitures of non-core assets.

“The core is pretty set, but what does move is technology,” True says. “We have gone from one-mile laterals to two-mile laterals to now three- and four-mile laterals and horseshoes. Those are the things that expand the core.”

Rigs at affiliated company True Drilling typically drill three- and four-mile laterals, he observes. In March, one was drilling a horseshoe lateral for a Williston customer. True Oil also has options for creative laterals on its holdings.

Outside the Williston, True Oil’s core assets are located in Powder River, and the company has properties in the portion of the Denver-Julesburg Basin straddling the Wyoming-Colorado border, as well as some Denver-Julesburg Basin assets east of Denver. Non-operated properties are located in Kansas and New Mexico.

In addition to True Drilling, other affiliates include True Pipe and Supply, Black Hills Trucking, product marketing wholesaler True Fuels, Bridger Pipeline, and Eighty-Eight Oil LLC, which operates the Gurnsey oil hub.

The proposed additions of gas takeaway from the Williston would prevent any oil drilling cutbacks for lack of associated gas outlets, True concludes.

Royalty Interests

Mesa Minerals Partners has historically focused its investment strategy on the Haynesville Shale play in North Louisiana and East Texas, as well as the Permian Basin in West Texas, across its three prior iterations. With the launch of its latest vehicle, Mesa Royalties IV, in early 2025, the firm sought to diversify its portfolio by adding a “third leg to the stool” through exposure to an additional oil-weighted basin.

For Mesa, the Williston Basin emerged as a compelling target, given its oil-rich profile, attractive estimated ultimate recoveries (EURs), consistent rig activity, and consistent rig count. “These attributes made the basin a natural fit for our royalty acquisition strategy,” says President and CEO Darin Zanovich.

Mesa’s most recent acquisition in the Williston includes approximately 5,800 net royalty acres (NRAs) purchased from Waveland Bakken Holdings. Since entering the basin last summer, the company has acquired more than 15,000 NRAs and has considerably grown basin-level cash flow.

“Prior to conducting our technical evaluation, we viewed the Bakken as a mature play that was less suited to a minerals acquisition strategy,” Zanovich notes. “However, recent well results—particularly those incorporating longer laterals and extended development—have demonstrated meaningful upside.”

Mesa evaluates royalty opportunities across the Williston but prioritizes assets operated by leading operators such as Devon Energy, Chord Energy, Chevron, Kraken Resources, and Continental Resources.

Mesa Royalties IV is supported by a $300 million capital commitment from NGP Capital and has rapidly assembled a diversified portfolio, including its Williston position, more than 12,000 NRAs in the Haynesville, and approximately 2,000 NRAs in the Permian. The new platform currently generates significant annual cash flow, with continued growth expected.

The Williston Basin’s EURs and other attributes make it a play of choice for Mesa Minerals Partners to acquire royalty interests on assets being developed by some of the basin’s top operators. The company’s latest Williston transaction includes 5,800 net royalty acres acquired from Waveland Bakken Holdings. Mesa started buying in the Williston last summer and has since acquired over 15,000 net royalty acres while growing basin cash flow to roughly $8 million annually.

Mesa’s prior vehicle, Mesa Royalties III, holds royalty interests in the Haynesville and Permian basins and produces approximately $70 million in annual cash flow from roughly 4,000 producing wells. Across the broader Mesa portfolio, asset exposure is evenly split between oil and natural gas.

Zanovich emphasized the strength of the Williston from a royalty owner’s perspective, citing predictable well performance, defined spacing, and operational efficiency. “Even in lower-price environments, the basin supports activity levels of approximately 30 rigs, with multi-well pad development driving capital efficiency. In higher price cycles like we are experiencing now, there is significant upside to both rig count and overall activity.”

Mesa also benefits from disciplined underwriting, as it does not assign value to unproven upside such as refracturing opportunities or infill drilling to replace early-generation horizontal wells. Longer term, the basin may also benefit from secondary recovery techniques, further enhancing value.

Additionally, the Williston’s development timeline reduces long-term execution risk on drilling pace relative to other basins. The play is expected to be largely developed within the next decade, and it offers a stable regulatory environment and relatively low political risk.

Unlike Texas and other states where public tax role databases enable rapid identification of mineral owners, title research in the Williston requires in-person courthouse work. This added complexity can deter less specialized buyers and creates an advantage for experienced groups like Mesa willing to spend upfront title dollars.

Mesa maintains relationships with more than 30 local acquisition agents, many of whom are based in North Dakota, making it one of the largest on-the-ground acquisition companies in the basin. The market for royalty minerals in the Williston remains highly competitive, with a wide range of valuations depending on asset quality. Transactions may include both producing (PDP) assets and undeveloped locations where lease bonuses have already been realized. Typical royalty lease terms range from 20% to 22.25%.

“We offer mineral owners pricing consistent with what we would pay institutional sellers, including oil and gas companies holding mineral or overriding royalty interests,” Zanovich says. “The market is highly efficient, and current conditions present a compelling opportunity for landowners to monetize their royalty interests.”

Mesa’s acquisition strategy is underpinned by a 13-person technical team comprised of reservoir engineers, geologists, land professionals, along with finance and accounting specialists—structured similarly to an upstream E&P organization—to rigorously evaluate and underwrite each investment.

Long-Lateral Inventory

The Williston’s largest acreage holder and producer, Chord Energy, continues to acquire assets and bolt-on acreage in its ongoing quest to expand long-lateral inventory across 1.3 million net acres in western North Dakota and eastern Montana.

Of the Houston company’s entire 10-year, low-breakeven inventory, 80% now includes longer laterals split between three- and four-mile horizontals, a goal the company met before the end of 2025, says CEO Danny Brown.

This year, four-mile wells will make up 40% of wells being turned to sales—up dramatically from only 5% in 2025. Average lateral lengths are expected to increase to 16,000 feet this year compared to ±13,000 in 2025.

Chord’s extensive, contiguous acreage is ideal for longer laterals to improve inventory and lower drilling and breakeven costs, which Brown says is down 10% year-over-year.

The company will spend $1.4 billion in 2026, running up to five rigs and two frac crews, to bring on up to 165 gross wells with average working interests of 75%. Although the footprint provides drilling options across the basin, work is weighted slightly to the western portion of Chord’s position.

Production of 277,000 boe/d is 57% oil. Brown says GORs are rising, as are takeaway options, with the outlook including the first segment of WBI Energy’s Bakken East Pipeline—expected to begin operations in 2029—and a Bison Xpress addition coming on line in May.

In addition to longer laterals, other efficiencies are enhancing operations. Improvements include 24-hour workover rigs, continuous rod-less pumping, and artificial intelligence-driven machine learning scaled to 99% of rod-lift wells. The company has experienced more than a 50% reduction in electrical submersible pumping cycle times and a 25% improvement in overall ESP failure rates.

Given an expansive position and trove of long-lateral inventory, there is little need for creative laterals, but Brown notes that U-shaped and other lateral designs are part of Chord’s toolbox if needed.

Since 2021, Chord has made five Williston acquisitions, the latest of which closed last fall: the purchase of 48,000 acres from XTO Energy in the Williston core. The company will continue to take a disciplined approach to mergers and acquisitions and bolt-ons to build repeatable middle Bakken inventory on conservative spacing, according to Brown.

“Obviously, we are aware of the full column that sits underneath our acreage position,” he concludes. “We are watching what others are doing in and out of the basin and see what we can apply.”

Slower Decline Rates

For non-operator Vitesse Energy, longer laterals mean lower well decline rates, reduced drilling and completion costs, and higher rates of return—whether from its organic non-op positions, acquisitions of Williston authorization for expenditures, or drilling on more than 5,000 operated acres from its acquisition of Lucero Energy in March 2025.

“The first-year production on a three- or four-mile lateral may look similar to a two-mile lateral, but the decline rate is much lower,” observes Ben Messier, director of investor relations and business development. “For a dividend model like ours, in which lower decline rates support our ability to return capital by reducing our maintenance capital expenditures, we are very happy to see the trend toward longer laterals.”

Chord Energy continues to expand its long-lateral inventory across 1.3 million net acres in the Williston Basin, with development increasingly centered on three- and four-mile horizontals to improve drilling efficiencies and lower costs. The Houston-based operator is allocating $1.4 billion in 2026 to run up to five rigs and two frac crews, targeting as many as 165 gross wells while advancing AI-driven technologies.

With headquarters in Greenwood Village, Co., Vitesse has more than 200 net locations across about 60,000 net acres, primarily in the Williston but also the D-J and Powder River Basins. Overall, assets include traditional working interests averaging 3-4% in more than 7,000 wells operated by players basinwide. The diversity means no one well or project can stymie company performance, Messier says.

Founded by former CEO and Chairman Bob Gerrity and backed by a $500 million commitment from Jefferies Financial Group, capital expenditures this year are guided to be $50 million-$80 million to hold production at around 17,000 boe/d.

The company continues to keep an eye out for potential acquisitions after buying Lucero, formerly known as Petroshale, which included assets in the basin core on the Fort Berthold Indian Reservation. The purchase of operated assets provides an additional target for capital and included two high-return drilled but uncompleted wells that have since been completed, Messier details.

In early March, Vitesse signed a definitive agreement to acquire for $35 million in stock non-operated assets in the Powder River Basin chiefly under operators EOG Resources and Continental Resources.

With refracs and long-lateral wells driving more value to the bottom line, the company continues to benefit from its participation in drilling and completion authorizations for expenditures. Last year, over half its AFE participations were in three- and four-mile wells.

In typical years, Vitesse participates in 7-10 net wells on a combination of organic AFEs from its non-op assets and AFEs bought over the course of the year. Vitesse typically bids AFEs at a rate of return well above its cost of capital, Messier says. Over the past four years on average, the company has spent $23 million buying AFEs and an additional $89 million on drilling and completion costs, which makes its 2026 capital plan of $50 million-$80 million exemplary of improving efficiencies in the basin.

The company bids on hundreds of such projects a year, winning 10-15% of them. Messier notes that its technical team gathers weekly to review extensive well and production information housed in its database to identify potential targets.

“People think of the Bakkens as a mature play, but we built the company targeting drilling spacing units that have a lot of upside potential and undeveloped inventory in them,” Messier remarks. “While natural gas constitutes nearly 40% of our total production, gas sales make up approximately 10% of our revenue. We are primarily an oil company but view any uplift to gas prices or production as icing on the cake.”

Bakken East Pipeline

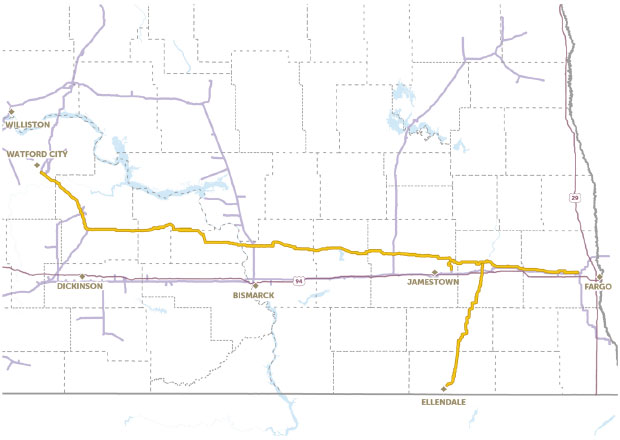

With natural gas production in the Williston Basin currently at 3.3 billion cubic feet per day and the basin expected to get gassier as gas-to-oil ratios continue to climb and as operators consider deeper, gas-prospective benches below the Bakken, WBI Energy is making plans for its 350-mile Bakken East Pipeline to transport more Williston Basin gas to market.

The regulated natural gas pipeline subsidiary of MDU Resources Group Inc. is proposing to build the pipeline in two phases from the core of the Williston Basin in McKenzie County, N.D., eastward to a compressor station near Mapleton just outside Fargo, says Mark Anderson, vice president of business development and marketing for WBI Energy.

With Williston gas production continuing to increase, WBI Energy is proposing the 375-mile Bakken East Pipeline. As planned, the pipeline will be constructed in two phases from McKenzie County eastward to a compressor station near Mapleton just outside Fargo. Once the project scope is finalized, based on firm volumes and associated contracts, the first phase in the west could include a 36- or 42-inch line, with the second phase a 30- or 36-inch line.

Already, Williston Basin gas plants connect to WBI Energy’s existing North Dakota system first developed long before the unconventional boom began.

Bakken East could connect to third-party pipelines such as Alliance Pipeline and Viking Gas Transmission, which serve gas markets outside North Dakota, says Anderson, a board member at the North Dakota Petroleum Council. The pipeline also would provide more gas for power projects to support data centers and other industries in a state that aggressively supports industrial growth.

“This project means good things for the Bakken long-term to ensure that natural gas takeaway capacity is not an obstacle to oil production, which is so important to not only our state because of tax revenue, but certainly for the country also,” Anderson states. “Across the entire state, we think it will foster economic development, whether that is new power generation or industrial growth, or just allowing communities to continue to grow and thrive.”

WBI Energy’s proposed project is the latest designed to move more Williston Basin gas to regional markets. Earlier in the year, Intensity Infrastructure Partners and Rainbow Energy Center LLC announced that firm transportation commitments are sufficient to start work on the first phase of the partnership’s 36-inch pipeline.

Anderson, who oversees pipeline capacity marketing at WBI Energy with the goal of having enough contractual commitments to support Bakken East development, says planning work began over a year ago. A nonbinding open season soon followed to gauge initial interest among shippers and end users. The Federal Energy Regulatory Commission approved WBI Energy’s request to use its pre-filing review process in February 2026 and the company held a binding open season, which concluded March 13, 2026. The WBI Energy team indicates it is pleased with the response to the open season and is actively negotiating contracts and determining final project scope.

Once the project scope is finalized, based on firm volumes and associated contracts, the first phase in the west could include a 36- or 42-inch line with the second phase a 30- or 36-inch line.

In the third quarter, the company plans to submit a Federal Energy Regulatory Commission 7(c) application required for authorization to build an interstate pipeline and related facilities, which would include new compressor stations and upgrades to existing facilities.

WBI Energy expects a FERC certificate in the third quarter of 2027. Construction of the 125-mile first phase could begin during the second quarter of 2028 and would be scheduled to enter service by the fourth quarter of 2029. The second phase would be installed and operational by the fourth quarter of 2030 under current plans.

Total pipeline cost has not been disclosed, but the company already has support from the state of North Dakota with a firm capacity commitment of up to $500 million—$50 million annually for 10 years—from the North Dakota Industrial Commission. Under state law, the commission can hold capacity on gas pipelines similar to a producer or end-user to boost project viability.

“We are very grateful for the proactive and meaningful support from the state of North Dakota,” Anderson says. “The state’s hope over time would be to release that capacity into the hands of a more commercial or traditional end-user or producer of natural gas.”

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.