Analysts See Significant Implications Of U.S. Supply Growth

By Charlie Cookson

WICHITA, KS.—Perhaps the most appropriate outlook for the dynamics of oil and gas in 2024 is a play on a familiar adage: The more things change, the more they are not going to stay the same.

Even a short list of common “group thinking” only a short time ago has been cast out the window by many forecasters, such as concerns that crude prices could go sky high, while a global shortage of natural gas brought on by Russia’s invasion of Ukraine could wreak havoc on natural gas supplies and logistics. One of the latest surprises unfolding today is that the unwinding of the Federal Reserve’s monetary policy tightening to fight an inflationary spiral, further flamed by the so-called Inflation Reduction Act, hasn’t created the expected crash landing in the form of a recession to remember.

Yet here we are, with relatively strong oil prices and a global resolve to maintain them, abundant natural gas, and what now appears to be a stronger-than-expected international energy market.

In November, U.S. Energy Information Administration data showed America’s producers set an all-time oil production mark of 13.2 million barrels a day, including shipping a record 4 MMbbl/d in crude exports. At the same time, the industry is running ahead of schedule in building out the needed infrastructure to correspond with new LNG export facilities. Indeed, the United States already has surpassed Qatar and Australia as the world’s largest LNG exporter, and another wave of new capacity is coming.

Can everyone grin and acknowledge American ingenuity?

As quoted in a New Year’s Eve analytical post in Forbes written by David Blackmon, Texas Alliance of Energy Producers Vice President Karr Ingham put it succinctly: “The United States is now producing more crude oil than any country ever has.”

The credit for that, according to Karr, goes to domestic oil and gas companies, especially independents, who are expanding production in the Permian Basin and other areas “for the benefit of the American people and the American economy.” He adds that operators are growing domestic production “with increasingly higher levels of efficiency and productivity.”

With differences in forecasts for supply and demand growth a given, the International Energy Agency’s December Oil Market Report acknowledged the go-it-alone April 2023 Saudi cut of 2 MMbbl/d, now extended to December 2024, as well as additional OPEC-plus supply cutbacks. Yet, against the backdrop of managed supplies, IEA said world oil demand in 2023 was on track to expand 2.3 MMbbl/d to close the year averaging 101.7 MMbbl/d, with an additional 1.1 MMbbl/d of demand expected to come from both OECD and emerging economies in 2024.

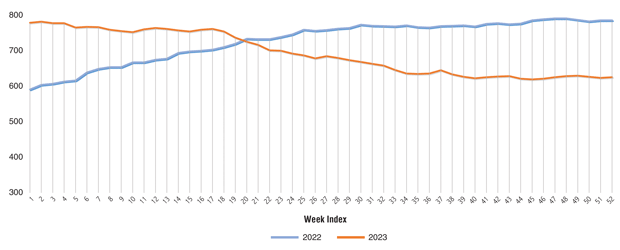

Weekly Drilling Rig Counts, 2022-2023

The Baker Hughes rig count was 588 at the begininng of 2022. A gradual yet steady pace of rigs turning to the right produced a year-end count of 779, up 191. A different story unfolded in 2023 as rigs fell from 779 to end the year at 622, down 157. Comparing the beginning of 2022 with the end 2023 shows a net gain of 34 drilling rigs.

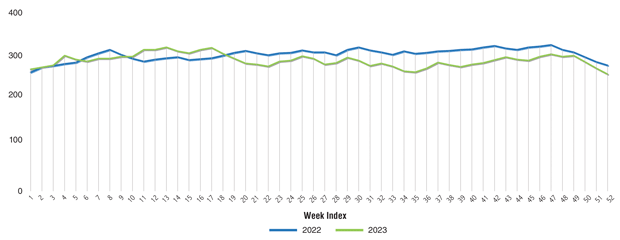

Weekly Frac Spread Counts, 2022-2023

Some of the same 2022 recovery story for drilling rigs holds true for frac spread counts. The gradual uplift from 244 at the beginning of 2022 resulted in a year-end count of 258. It should be noted, however, that many drilling crews keep working during year-end holidays, while many frac crews take a break. Removing the year-end shutdown and subsequent startup shows that frac crew counts were closer to a 275 level during 2022, hitting a high of 300 on Nov. 23. Nevertheless, a year-to-year comparison shows frac spreads were lower in an approximate range of 20-30 through most of 2023, compared with 2022.

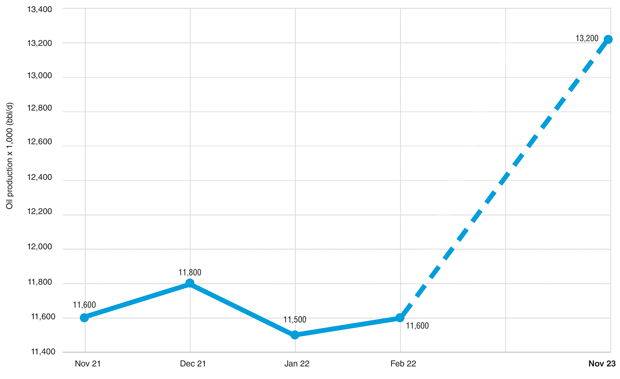

U.S. Oil Production, November 2021-November 2023

In a demonstration of ramping U.S. production in a compressed period and with fewer drilling and frac crews, the U.S. Energy Information Administration’s February 2022 production data totaled 11.6 million barrels a day. November 2023 set a record of 13.2 MMbbl/d which produced a gain of 1.6 MMbbl/d.

For its part, OPEC sees a higher addition of 2.25 MMbbl/d in new demand in 2024, and continues to signal its intention to balance market share concerns with a strategy to maintain current crude oil prices. The December IEA OMR is telling. It states that, while U.S. supply growth continues to defy expectations, production offshore Brazil and Guyana are also pushing to record highs, adding an exclamation mark to OPEC’s demonstrated supply-side discipline.

An end-of-year Reuter’s survey of 30 forecasts from economists and analysts resulted in an assessment that Brent crude would average $84.43/bbl in 2024. There are crude oil price contrarians, and even the price bulls cite downside risks of further geopolitical turmoil as well as lackluster growth from the sleeping demand giants of China and Japan. Indeed, they may be in the same camp as those expecting an oversupply of domestic natural gas and surprising resilient global natural gas stocks to keep a lid on the likelihood of meaningfully higher natural gas prices during the next several months. But they are hard to find.

In Bank of America’s “Year of the Landing” reports issued in late November, Candace Browning states, “We expect 2024 to be the year when central banks can successfully orchestrate a soft landing, although we recognize that downside risks may outnumber the upside ones.” In that report, head of commodities and derivates research, Francisco Blanch, sees oil demand growth at the same 1.1 MMbbl/d as IEA, yet with Brent and West Texas Intermediate benchmarks averaging a healthy $90/barrel and $86/barrel, respectively.

Although Goldman Sachs trimmed its November projections of 2024 Brent crude prices in the $80-$100/bbl range by $10/bbl in December, that still leaves Brent between $70 and $90/bbl, with the caveat that it may peak at $85 in June.

Industry Dynamics

One mantra that has been repeated at AOGR throughout its 65-year-history is that there is no such thing as a “typical” independent oil and gas producer and operator. AOGR editors grapple with the supply and demand scenarios and resulting commodity pricing year-round. We also assess capital trends, likely drilling and well completion activity levels, technology game changers—and today—even the likelihood for a rebound in startups and a resurgence in acquisition and divestiture dealmaking. An upswing in asset A&D activity typically follows the huge corporate merger and acquisition deals that occurred as 2023 wound down.

We are struck with the observation that we may need to expand the observation to the tune of “There is no such thing as a typical major integrated company.” The following deals and insights can hold significant ramifications and asset trickle-down effects for the upstream industry in the year ahead.

ExxonMobil’s blockbuster acquisition of Permian-stalwart Pioneer Natural Resources was met with significant press attention and plenty of excited commentary from industry analysts. That included those companies and individuals directly involved in M&A advising and the inevitable company-to-company A&D strategies crucial to the industry’s ebb and flow and the ongoing success of independent operators, in particular.

Early analysis from Reuters’ U.S. Energy Analyst Sabrina Valle put a personal spin on the all-stock deal by ExxonMobil, the world’s largest investor-owned oil company by revenue and market capitalization, to purchase Pioneer Natural Resources, one of the leading publicly owned independent shale players, in a deal valued at nearly $60 billion. In a report, Valle shared comments from a resurgent Darren Woods, chief executive officer of ExxonMobil.

“We basically closed this deal fairly quickly,” Woods stated, noting it was a win-win for ExxonMobil. Analysts assessed that ExxonMobil was paying a relatively small 16% premium to Pioneer’s unaffected share price, while the planned retirement of Pioneer’s founder and chief executive, Scott Sheffield, could let shareholders benefit from the deal’s cost and revenue synergies by giving them more than 10% of the combined company.

According to a separate report, the merged company could add 700,000 barrels of new oil equivalent per day to its upstream production, which Statista pegged at 2.4 MMbbl/d and 8.3 billion cubic feet of natural gas a day worldwide in 2022. The global major targeted Permian “pure player” Pioneer for its extensive leasehold in the Midland sub-basin of West Texas and its deep technical know-how in the largest petroleum-producing province in the United States.

Industry observers suggest Chevron’s acquisition of Hess Corp., on the other hand, is more complicated and based on an entirely different rationale, according to analysts. Market observers cite a multitude of benefits to Chevon, starting with a multi-billion dollar tax shield. Reuters quoted Donald Williamson of American University’s Kogod School of Business: “The Hess losses (loss carry-forward) will let Chevron lower its tax rate significantly for several years.”

Hess Corp. also holds legacy assets throughout the Williston Basin, and opened the door for Chevon to increase its Bakken presence while gaining a significant interest in the ExxonMobil-operated Uaru oil field offshore Guyana. Still in its infancy, the $12.7 billion Uaru development is located in the Strabroek Block. According to S&P Global, Guyana will have the world’s fastest-growing economy in 2024, thanks to the trickle-down economic effect brought on by one of the latest world-class offshore discoveries.

Fast-forward to the early January announcement of a $17 billion merger of Southwestern Energy and Chesapeake Energy. Although it may be a more traditional alliance of companies seeking economy of scale and technical proficiencies, it can certainly have huge ramifications for smaller companies with nearby acreage interested in picking up strategic assets. As always, properties that may be beneath the bar of excellence for the management of the combined companies are prime targets for smaller players watching the A&D market for new prospects.

To our readers who are key to the health of the economy, and who are already immersed in solving challenges and identifying opportunities with the optimism contagious throughout this great industry, we say: Enjoy the Ride!

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.