Foundational Principles Drive 50 Years Of Success, Position Devon For Future

By Danny Boyd, Special Correspondent

OKLAHOMA CITY–The ultimate proof of concept in the oil and gas industry is simple: staying power. The ups and downs of commodity price cycles tend to be more cruel than kind, and in a business where the only constant is constant change, only the best stand the test of time.

Welcome to the club, Devon Energy Corp.

This year, Devon celebrates its golden anniversary, entering a select circle of independent operators. From a meager start as a father-and-son team with little more than a grand idea, Devon Energy has become one of the industry’s true blue bloods. Over the years, it has seen play concepts, technology fads, financial strategies, business cycles and competitors come and then watched them go. Through it all, Devon has prospered by being smart, innovative, opportunistic and nimble enough to stay ahead of the curve, yet never getting so far out front that it exposed its flanks.

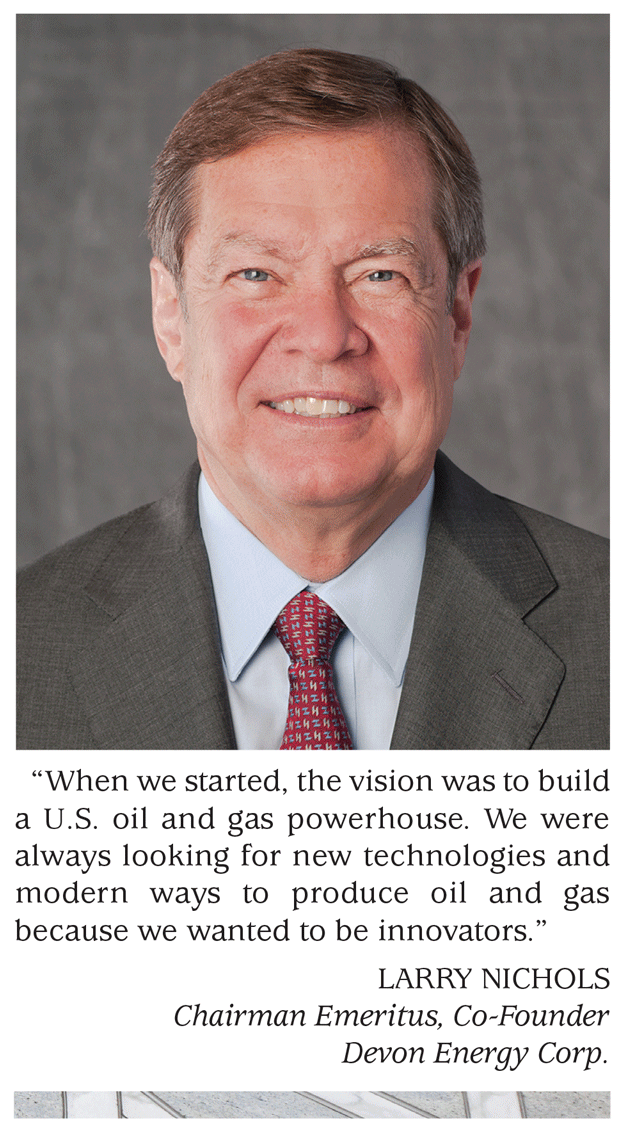

Chairman Emeritus Larry Nichols, who co-founded the company with his father, John, in 1971, says that reaching the 50-year milestone demonstrates that Devon’s business model can weather any storm.

“The economy is going to give you bad hits from time to time, but nevertheless, you come out better and stronger than you were at the start and you can only demonstrate that by the history of having actually done it,” he says. “We have people here who have done that, which increases the likelihood that they will be able to do it again in the future.”

While nothing in this business is ever certain, Devon has proven time and again that it has the people, assets, strategy, and technology to withstand the hits and somehow come out on top. Even from its earliest days, Devon was built on a different kind of thinking about the business, and how to grow long-term value.

“When we started, the vision was to build a U.S. oil and gas powerhouse,” Nichols reflects. “We were always looking for new technologies and modern ways to produce oil and gas because we wanted to be innovators.”

By the time John Nichols passed in 2008, the company had completed a series of mega-acquisitions that had catapulted it to the top of the list of independent producers. But “the Barnett Shale deal” that Devon closed in 2002 to acquire Mitchell Energy was the move that completed its metamorphosis from a family-owned small business to a Wall Street darling with a portfolio rivaling the biggest names in the industry. Devon cracked the Fortune 500 that same year and was well on its way to becoming the largest U.S.-based independent.

Powerhouse status accomplished.

Impressive Story

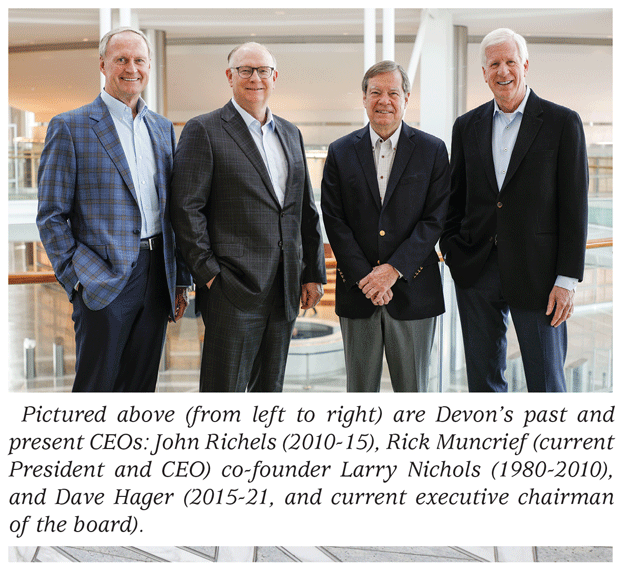

But it was through a lot of hard work, sheer force of will, and innovation–at times out of necessity–that a startup with no assets was transformed into an industry dynamo with a starring role in the unconventional oil and gas revolution, points out President and Chief Executive Officer Rick Muncrief.

“When you think about the company that John and Larry Nichols started, and the fact that it had little money or assets, and you see how they built it into a company with a truly global reach on different continents, it is a very impressive story,” he says.

Devon’s culture of continuous innovation and high expectations was established by the Nichols long before Devon became a publicly traded global juggernaut through a series of mergers, acquisitions and the drill bit.

A half century after its founding in and fresh off a significant “merger of equals” with WPX Energy, Devon is looking to advance its competitive edge through drilling and completion techniques in the Delaware Basin and other core operating areas to support an industry-first variable dividend. The work is being done amid plans to achieve net zero greenhouse gas emissions for Scopes 1 and 2 by 2050 and cut methane emissions intensity by 65 percent by 2030.

Despite the magnitude of the challenges, the company is positioned to achieve its ambitious goals, says Executive Chairman David A. Hager, a former Devon president and CEO.

“Devon is in a very strong position to have an incredibly bright next 50 years,” Hager enthuses. “We are now positioned as one of the strongest oil and gas companies in North America with a very strong asset base. We are executing at a very high level in our operations and in all of our groups throughout the company. I think it shows that this company has been progressive from the beginning and is going to continue to be progressive with a strong foundation in our traditional business that will allow us, when appropriate, to transition into other opportunities.”

Building Something Better

Devon’s achievements are as much the result of integrity and the dedication of frontline employees as company leadership, insists Muncrief, who was CEO at WPX Energy prior to the January 2021 merger. Indeed, employees from legacy Devon and WPX continue to demonstrate a willingness to make sacrifices and embrace an organizational mindset dedicated to continual improvement that will further fuel the company’s success, he adds.

“It is a testimony to the quality of the people and the cultures, and the recognition that, even though you are good, you can build something better,” he comments. “I am very proud of how the companies have come together. Devon was in a very strong position and had a positive outlook prior to the WPX merger; we have been able to further strengthen the company. Put the two together, and I think we have a great outlook and a strong company and culture.”

Devon’s winning mindset was birthed in financial innovation that began when John Nichols, an accountant, became the first to register an oil and gas drilling fund with the U.S. Securities & Exchange Commission in 1950. John and Larry–then a practicing attorney who had clerked for both U.S. Supreme Court Chief Justice Earl Warren and Associate Justice Tom C. Clark, and worked for William Rehnquist when Rehnquist was a U.S. assistant attorney general–launched Devon with a tax loss carryforward, zero assets or proved reserves.

The newly established company appealed to European investors who wanted a piece of the action in the American oil patch. It was hardly a typical financing strategy, but with overseas capital backing, the Nichols were in business.

The spirit of financial innovation continues. In February, Devon announced the industry’s first variable dividend. The payout will be up to 50 percent of net free cashflow after funding the base dividend, capital expenditures/operations, and paring down debt, Muncrief says.

On March 31, shareholders received a variable dividend of $0.19 per share on top of a fixed dividend of $0.11. The second variable dividend at the end of June included $0.23 per share on top of the fixed distribution.

“Free cash flow separates the winners from the other folks right now, and quite honestly, we are winning and leading the industry with a variable dividend,” Muncrief comments. “Devon has paid a fixed dividend for 28 consecutive years, and as the only company implementing a variable dividend, we are challenging other companies that could be doing that. It will help the entire sector show how much discipline we have and how we are getting additional capital back to shareholders who have supported us through some arguably lean times.”

Climbing To The Top

Innovation began early on the operations side as well. During the 1970s, when many of its peers were looking at venturing into the international and offshore arenas, Devon focused on acquiring producing properties in established onshore domestic fields and applying new ideas and technology–an approach that allowed the company to expand methodically for almost 20 years, Nichols says.

In the San Juan Basin in the late 1980s, innovation at Devon’s Northeast Blanco Unit (NEBU) led to exploration of the basin’s coalbed methane formations previously considered a nuisance to operators tapping into deeper oil and gas reserves. The company competed successfully with larger rivals bent on getting the upper hand, and in the process transformed NEBU into an historic natural gas producer that helped transform the San Juan from an aging play to a premier natural gas basin, Nichols recalls.

Growth took a giant leap forward after the company went public in 1988. During the 1990s and beyond, a series of mergers and acquisitions expanded Devon’s reach off shore, at home and abroad. The strategy began with the 1992 purchase of Hondo Oil & Gas for $122 million and continued with some of the industry’s most noteworthy deal making over three decades, including:

- A $250 million acquisition of Kerr-McGee’s North American onshore oil and gas properties in 1996 that nearly increased its reserves by 46%;

- A $750 million acquisition of Northstar Energy in 1998, making Devon one of the 15 largest U.S. independents;

- A $2.6 billion acquisition of PennzEnergy in 1996, giving Devon a significant position in the Gulf Of Mexico;

- A $3.5 billion merger with Santa Fe Snyder in 2000, making Devon a “top five” independent and expanding its international holdings;

- A $4.6 billion acquisition of Anderson Exploration in 2001, establishing Devon as the third-largest independent gas producer in Canada;

- The landmark $3.5 billion acquisition of Mitchell Energy in 2002;

- A $5.3 billion merger with Ocean Energy in 2003 that created the largest U.S.-based independent producer;

- A $2.2 billion acquisition of Chief Oil & Gas’s Barnett Shale leasehold in 2006;

- A $6.1 billion acquisition of Eagle Ford player GeoSouthern Energy Corp. in 2014;

- A $1.9 billion acquisition of Felix Energy and its STACK play holdings in 2016; and

- A merger with WPX Energy in 2021 to achieve enhanced scale, improved margins, higher free cash flow, and the financial strength to accelerate shareholder returns.

Leading The Revolution

Shortly after closing on the cash and stock purchase of Mitchell Energy and its Barnett Shale assets in North Texas, Devon began developing its in-house mastery of the art and science of slickwater hydraulic fracturing techniques. The late George Mitchell, founder of Mitchell Energy, devoted much of his professional energies over his long and esteemed career to perfecting the right frac recipe for gas shale formations.

“George Mitchell and Mitchell Energy discovered the use of slickwater in hydraulic fracturing of vertical wells,” Muncrief recounts. “And then Devon became the first to combine hydraulic fracturing with horizontal drilling, and that was the real breakthrough that led to the Shale Revolution, first in natural gas and then crude oil throughout the country, and in fact, throughout the world. It has totally revolutionized the entire industry.”

The industry’s transformation fueled a surge of drilling and production in unconventional plays around the country, including gas shales in the Appalachian Basin and stacked tight oil plays in the Permian Basin, which not only reversed declining U.S. oil and gas output, but vaulted daily production of both to all-time highs.

Beginning in 2010, Devon refocused on top-tier lower-48 tight oil plays by selling all of its offshore and international holdings, including assets in Brazil, Azerbaijan, Canada, and the Gulf of Mexico. It also began rationalizing its domestic holdings, spinning off non-core properties in the Rockies, Mid-Continent, Texas, and northern Louisiana. The company’s move to recast itself as a “U.S. oil growth company” was finalized in 2020 after it sold its Barnett operations to Denver-based Banpu Kalnin Ventures.

Merger Of Equals

The deal making not done, in January, Devon and WPX Energy–the product of a spinoff from Tulsa-based Williams Cos. in December 2011–joined forces through a merger of equals. The agreement integrated the two Oklahoma companies, including boards and executive teams, and created a huge 400,000-net acre position in the Delaware Basin, which Muncrief calls Devon’s new crown jewel.

The company is studying different completion techniques used by legacy Devon in the northern Delaware Basin of southeastern New Mexico and by WPX farther south, he says. The company could adopt one of the methods to use throughout its position or find a better way to fully exploit oil and gas from the Bone Spring, Wolfcamp, Avalon, Delaware and Leonard formations. Devon is currently running 13 rigs in the basin, Muncrief says.

“We are having really good discussions in a multitude of areas and I am very encouraged that we are going to continue to improve our capital efficiency and increase our technical understanding,” he remarks. “Investors are going to win.”

Its Delaware Basin position will take the company far into the future, he says, adding that the outlook is bright despite initial market misgivings over Devon’s large federal acreage holdings in New Mexico after the Biden administration temporarily froze new permits from the U.S. Bureau of Land Management, which is now issuing them again.

“I think the market was overly concerned about whether we could continue development with the changes in administration,” Muncrief offers. “We felt, without a doubt, that we could and that is exactly what is happening. We have more than 500 existing permits. We are working that backlog now and are still getting permits. I think the BLM has done a great job.”

Winning Combination

The Devon-WPX merger will help further demonstrate operational and financial stability needed by service companies acutely subject to the industry’s ups and downs, he adds.

“You have to have strong cash flow and a strong balance sheet, and creative people who are always trying to do innovative things,” Muncrief says. “That is exactly what we have, and I think it is a winning combination when applied to top-tier assets.”

Great assets, efficient capital allocation, adequate cash on hand, and overall financial discipline together allowed Devon in June to pay down $1.2 billion of debt several years before it was due, Muncrief reports, as the company works to keep production relatively flat. Buttressing Devon’s financial outlook is a decreasing amount going forward of hedged production at lower prices, which will further bolster free cash flow at today’s higher price levels, he says.

“We are being very disciplined,” Muncrief relates. “In the old days, we would have put that money to the drill bit and just grown. But that is not what the market wants and not what the market needs right now.”

While the lion’s share of the company’s net oil production of 280,000-290,000 bbl/d (400,000 bbl/d gross) are from the Permian, Devon will continue to rely on production from other basins, he explains. From 45,000 to 50,000 bbl/d come from the Williston, a former WPX holding. WPX also brought assets in the Powder River and Anadarko basins to the table from a 2015 acquisition of Felix Energy.

“Every one of these assets plays a different role at this point in time,” Muncrief explains. “For instance, the Powder River Basin is quite different from the Bakken in that the Bakken is very mature. The Powder River is very immature, but the Bakken is spinning out a lot of free cash flow at these commodity prices, so it is really nice to have. We do not have to spend a lot of capital there right now. It is an area where we will continue to focus and where the industry has been forced to flare more because of midstream constraints. We are going to focus on capital efficiency and improving flaring numbers.”

Devon’s Eagle Ford position includes a consistent operation in a joint venture with BPX, while the company’s large Mid-Continent holdings–including 300,000 acres in Oklahoma–is a “nice wet gas option that provides solid revenues from premium pricing,” Muncrief describes. That position should prove to be especially beneficial amid talk of a growing need for additional natural gas-fired power plants to generate power to augment alternative sources, he adds.

Innovations that have revitalized drilling and production in the lower-48 have a deep Oklahoma imprint, says Muncrief, an Oklahoma native whose father worked in the industry and whose two grown children do as well.

“I think about how Oklahoma-based Devon, Chesapeake Energy and Continental Resources all have a rich legacy of rewriting the books in a lot of ways,” he says. “There is a creative, entrepreneurial spirit in Oklahoma.”

Embracing ESG Discussions

Despite concerns about policy and regulatory impacts from the climate change debate, Devon is embracing the ESG discussion, he says. On June 21, the company announced new environmental performance targets to reduce the carbon intensity of its operations and minimize freshwater use.

In addition to its goal of achieving net zero greenhouse gas emissions for Scopes 1 & 2 and reducing methane emissions, Devon plans to achieve flaring intensity of 0.5% or lower by 2025 and eliminate routine flaring by 2030. The company also plans to continue advancing its water recycling rate and use 90% or more nonfreshwater for completions in its most active operating areas of the Delaware Basin, according to Muncrief.

Under its new targets, Devon will continue to evaluate how to engage stakeholders upstream and downstream of operations to improve ESG performance. By 2023, Devon’s contractors who perform work on company locations will begin undergoing annual evaluations to assess their ESG performances in key areas.

“It is not just energy, but all companies and sectors are thinking about ESG. We must embrace it and be thoughtful, strategic and smart about things,” Muncrief says. “We are going to focus year after year on achieving even better ESG scores and impacts on emissions and governance as a company. We are also going to be communicating the great things we are doing for society. We are not running from the discussion. We welcome it. Some in the industry may be frustrated, but we are not. We want to know what people are thinking. The best thing we can do is stay at the table, keep talking through it and communicate the value we bring to peoples’ lives every day.”

Hager affirms Devon’s commitment to be a good environmental steward and act in the interests of communities, investors and employees alike. Devon’s story will continue to be written not only in the present and not merely by pausing to reflect on how far it has come since 1971, but by keeping an eye on where it is going during the next 50 years, he says.

“There are very few companies in our industry that survive for 50 years, so that is the most fundamental thing,” Hager says. “Not only have we survived, but we have done it with integrity. We have done it by being a good neighbor in our community. Any of our employees can proudly say, ‘I work at Devon,’ and have it mean something positive to the community and to our neighbors.”

Muncrief concludes, “Looking back at Devon’s last 50 years gives us a lot to be proud of. I am excited and humbled to lead the company into its next stage, and am confident that Devon’s culture of integrity, focus on forging strong relationships and acting courageously will continue yielding strong results for all of our stakeholders.”

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.