Independents Predict Double-Digit Increase In Drilling Activity For 2008

By Bill Campbell

Don’t look for America’s drilling rigs to stop turning to the right anytime soon–especially those searching for crude oil.

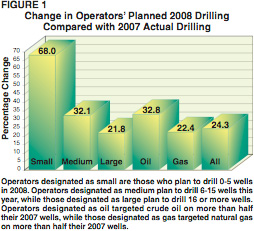

For the sixth consecutive year, respondents to The American Oil & Gas Reporter’s annual Survey of Independent Operators have predicted a double digit year-on-year increase in their drilling activity, projecting they will drill 24.3 percent more wells this year than they did in 2007.

Operators who are primarily interested in finding oil (survey respondents who indicated they targeted crude oil with more than half of their 2007 wells) are the most upbeat, planning a nearly 33 percent increase in drilling. But gas-well drillers (those who targeted natural gas with more than half their 2007 wells) aren’t exactly despondent, forecasting their own 22 percent increase in 2008 drilling

The American Oil & Gas Reporter mails the Survey of Independent Operators annually in November to oil and gas producers nationwide, selected randomly from the magazine’s circulation list. No attempt is made to identify survey respondents, and The Reporter’sstaff compiles and analyzes the data. The Survey of Independent operators does not account for dry holes, and merely asks operators what the intended target is when a well is spudded.

The 2008 survey depicts an independent oil and gas industry realistic in its price expectations and seemingly confident that the infrastructure is in place to meet its goals. At a time when the light-sweet crude oil contract on the New York Mercantile Exchange was flirting with $100 a barrel and posted prices in much of the nation were north of $80, survey respondents said they were basing their 2008 drilling plans on a very modest $66.62 a barrel.

Price projections were fairly consistent throughout respondent categories. Crude oil price expectations ranged from a low of $65.76 a barrel among oil-well operators to a high of $67.67 a barrel for gas-well operators, with small-category survey respondents (those who indicate they will drill 0-5 wells in 2008) coming in at $67.04 a barrel, medium-category respondents (those who indicate they will drill 6-15 wells in 2008) projecting $66.29 a barrel, and large-category respondents (16 or more wells in 2008) estimating $66.21 a barrel.

The natural gas prices on which respondents indicate their 2008 drilling plans are based are a little more in line with prices at the time. During a survey period in which the NYMEX natural gas near-month futures contract ranged between $7.55 and $8.00 an MMBtu, survey respondents as a whole signaled they were anticipating $6.28 an Mcf during the coming year. This ranged from $5.53 an Mcf for the oil-well driller category of respondents to $6.56 an Mcf for the gas-well category, with the small-driller category coming in at $6.20 an Mcf, medium-driller category at $6.08 and large-driller category at $6.50 an Mcf.

Continuing Upward

The 2008 Survey of Independent Operators is almost a mirror image of the 2007 survey in that a year ago–following 10 months of declining crude oil prices–natural gas operators were much more optimistic than their crude oil brethren, predicting a 40 percent increase in 2007 activity compared with only a 24 percent increase by oil operators (The Reporter, January 2007, pg. 45).

This year, after a 10-month upward trek in crude oil prices, survey respondents primarily interested in drilling oil wells project a 33 percent increase in drilling activity (Figure 1) compared with only 22 percent for gas-well drillers. As usual, the small-category of survey respondents leads all categories, predicting a 68 percent increase in 2008 drilling. However, it should be noted that because of the small number of wells drilled by the small-category respondents, a relatively small increase in total drilling translates to a large percentage increase.

Small-category respondents drilled an average of 1.7 wells in 2007 and plan to drill 2.9 wells in 2008, compared with an average 6.9 wells in 2007 and 9.2 wells in ’08 for medium-category respondents and 54.3 wells in 2007 and 66.1 wells in ’08 for large-category respondents.

Medium-category respondents, who tend to be more “oily” than large-category drillers, are projecting a 32 percent increase in 2008 activity while the large category indicates a 22 percent bump in drilling.

The “average” respondent to the Survey of Independent Operators drilled 20.4 wells in 2007 and anticipates drilling 25.4 wells this year. The average respondent targeted natural gas with 74.5 percent of his wells last year, but anticipates a 3.0 percentage point shift toward oil this year. That holds true even for gas-well drillers, who say they aimed for natural gas on 95.5 percent of their 2007 wells, but will do so with only 92.7 percent in 2008.

As in years past, the more active drillers tend to be more focused on natural gas. The large category of survey respondents say they were drilling for natural gas with 78.8 percent of the 2007 wells, but will do so with only 76.7 percent of their 2008 wells. For medium-category respondents, 53.4 percent of their 2007 wells were seeking natural gas while 48.9 percent of their 2008 wells will target gas. Small-category respondents report they were drilling for gas on 38.0 percent of their 2007 wells and will do so with 35.7 percent of their ’08 wells.

Oil well drillers are more inclined to go exploring than their gas counterparts. Respondents drilling for oil more than half the time report 30.2 percent of their 2007 wells were exploratory and say 29.1 percent of their ’08 wells will be wildcats, while gas-well drillers were wildcatting on only 8.5 percent of their ’07 wells and say only 7.1 percent of their ’08 wells will be exploratory.

The average depth of wells drilled by all respondents in 2007 was 5,038 feet, and is projected to decline to 4,983 feet in 2008. This slight shift to shallower wells held through all categories of survey respondents except for oil-well drillers, who reported the shallowest average depth in 2007 at 4,559 feet and say it will rise to 4,795 feet in 2008.

Drilling And Spending

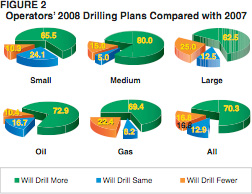

Even though oil-well drillers are projecting a 10 percentage point larger increase in 2008 drilling than gas-well drillers, the difference is in the number who anticipate drilling fewer wells this year than last. While 73 percent of oil-well drillers say they will drill more wells this year (Figure 2), 69 percent of gas-well drillers say they will drill more wells this year. But while only 10 percent of oil-well drillers say they will drill fewer wells in ’08, 22 percent of gas-well drillers expect to cut back.

The step back is greatest among the most active drillers. One-fourth of large category survey respondents say they will drill fewer wells in 2008 than they did in 2007, while only 15 percent of medium category respondents and 10 percent of small category respondents say they will drill fewer wells, while 80 percent of the medium category and 66 percent of the small category respondents expect to drill more wells, compared with 63 percent of the large category.

Overall, 70 percent of all survey respondents say they will drill more wells in 2008 than they drilled in 2007, 13 percent expect to drill the same number, and 17 percent say they will drill fewer.

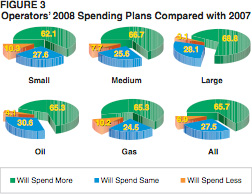

Spending plans don’t quite keep pace with drilling. Only 66 percent of all survey respondents say they expect to spend more drilling wells in 2008 than they did in 2007 (Figure 3), while 28 percent say they will spend the same and 7 percent expect to spend less.

The oil and gas categories of survey respondents are dead even with 65 percent of both projecting an increase in spending, although 10 percent of gas-well drillers say their drilling budgets will decline this year compared with only 4 percent of oil-well drillers.

Size apparently counts when it comes to projecting drilling budgets because 69 percent of the large-category respondents say they will spend more this year, compared with 67 percent of the medium category and 62 percent of the small category. Even though a quarter of the large-category respondents say they expect to drill fewer wells this year, only 3 percent anticipate smaller drilling budgets, compared with 10 percent of the small category that say they will spend less and 8 percent of the medium category.

Price Sensitivity

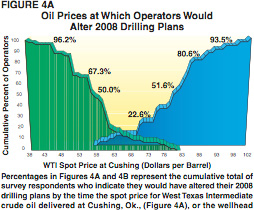

When there is more than a $25 cushion between the prevailing crude oil price and the target price on which independent producers are formulating their drilling plans for the coming year, there apparently is little prices can do to induce more drilling. When asked at what dollar a barrel amount above their target oil price survey respondents would increase their 2008 drilling programs, fewer than half said there was any price that would cause them to drill more wells.

Ironically, of the 44 percent who did answer the question, most indicated a price below prevailing prices during the survey period! Indicating that their 2008 drilling plans were based on a crude oil price (West Texas Intermediate at Cushing, Ok.) of $66.62 a barrel, 51.6 percent of survey respondents said a price of $81 a barrel would cause them to drill more wells (Figure 4A). Two-thirds (67.7 percent) flagged $84 a barrel as the price at which they would increase their 2008 drilling programs, while by the time prices rose above the $90 a barrel prevailing at the time, more than 90 percent of survey respondents said they would drill more wells.

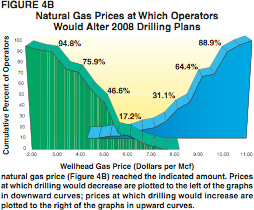

There was a little more price sensitivity on the downside, with about a third (32.7 percent) saying $60 a barrel would cause them to cut back their 2008 drilling plans. At $57 a barrel, exactly half would reduce the number of wells they planned to drill this year, and at $55 a barrel, 67.3 percent would cut back. At $50 a barrel, 86.5 percent say they would drill fewer wells, and at $45 a barrel, 96.2 percent say they would drill fewer wells. For natural gas, where survey respondents indicate their 2008 plans are based on a price of $6.28 an Mcf, anything above $8.00 an Mcf elicits a positive response. Nearly a third (31.1 percent) of survey respondents say they would increase their

2008 drilling programs at a natural gas price of $8.00 an Mcf (Figure 4B). That number grows to 64.4 percent at $9.00 an Mcf and to 88.9 percent at $10.00.

Looking on the downside, $5.00 an Mcf is the price that would signal trouble for a great many U.S. independents. While only 17.2 percent of survey respondents say they would cut back their 2008 drilling programs at $5.50 an Mcf, 46.6 percent would do so at $5.00, and 58.6 percent would drill fewer wells at $4.50 an Mcf. If natural gas prices fell to $4.00 an Mcf, 75.9 percent of survey respondents say they would reduce their 2008 drilling programs, and 94.8 percent would cut back at $3.00 an Mcf.

About a third (32.0 percent) of survey respondents indicate they use financial instruments to hedge a portion of their production. Among hedgers, 24.2 percent say they hedge 1-25 percent of their production, 36.4 percent hedge 26-50 percent, 30.3 percent hedge 51-75 percent, and 9.1 percent hedge 76-100 percent.

Large and gas-well drillers are more likely to hedge than their smaller or oil counterparts. Nearly three-fifths (59.4 percent) of the large-category respondents say they hedge, compared with only 17.2 percent of the small category and 20.0 of the medium category. Among the large-category respondents who say they hedge a portion of their production, 78.9 percent indicate the amount they hedge is between 26 and 75 percent.

Among gas-well drillers, 46.0 percent of survey respondents say they hedge a portion of their production, of which 69.6 percent hedge between 26 and 75 percent. Only 16.3 percent of oil well drillers say they hedge a portion of their production.

Positive Factors

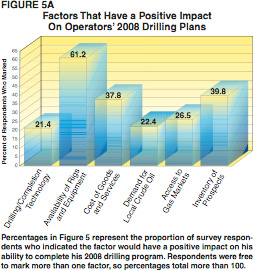

In an apparent tip of the hat to the service and supply industry’s ability to put the equipment and supplies needed to drill more wells into the field, survey respondents most often picked the availability of drilling rigs and equipment from a list of six factors that might have a positive impact on their ability to complete their 2008 drilling programs.

As shown in Figure 5, 61.2 percent of survey respondents say they expect the rigs and equipment they need to complete their ’08 drilling programs to be available. Furthermore, the availability of rigs and equipment was picked by the greatest number of respondents in all five survey categories. Small-category respondents were the most upbeat about their ability to get rigs and equipment with 70.4 percent indicating this would have a positive impact on their 2008 operations, compared with 57.9 percent of the medium category and 58.1 percent of the large category.

In a related question, 29.7 percent of all survey respondents say they expect lead times for drilling rigs and equipment to shorten in 2008 compared with 2007, while 60.4 percent expect them to remain the same. Perhaps indicating they experienced greater problems obtaining the necessary hardware in the past, 31.0 percent of the small-category respondents say they expect wait times for rigs and equipment to decline this year, compared with 20.0 percent of medium-category respondents who expect shorter lead times and 26.7 percent of the large category.

Within the oil and gas categories, gas-well drillers are most upbeat about the lead times, with 36.0 percent of gas-well drillers expecting shorter waits, compared with 20.8 percent of oil-well drillers.

Back on the factors that will impact their ability to complete their 2008 drilling programs, their inventory of drilling prospects came in second among survey respondents as a whole, with 39.8 percent flagging this as a positive influence. Gas-well drillers were most upbeat about their prospect inventories, with 47.9 percent signaling this as a plus, compared with only 31.9 percent of oil-well drillers. Their inventory of prospects was the second-most positive factor for gas-well drillers, while it ranked only fourth among oil-well drillers.

Third among all survey respondents was the cost of goods and services (Figure 5), followed by access to gas markets, demand for local crude oil, and drilling and completion technology. Large-category respondents were most likely to find a positive influence in technology advances, with 41.9 percent marking them as having a positive influence, compared with only 11.1 percent of small-category respondents and 10.5 percent of medium-category respondents.

Next to the availability of rigs and equipment, the small-category respondents were most likely to see the cost of goods and services (48.1 percent) as a positive factor, followed by demand for local crude (29.6 percent). For the medium category, prospect inventory was second at 50.0 percent, followed by the cost of goods and services at 36.8 percent. In the large category, prospect inventory was second (45.2 percent), followed by a tie between drilling and completion technology, and access to gas markets at 41.9 percent.

For gas-well drillers, prospect inventory was second at 47.9 percent and access to gas markets was third at 45.8 percent. For oil-well drillers, the cost of goods and services was second at 42.6 percent, followed by demand for local crude at 34.0 percent.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.