NGLs Present Opportunity To Create Value In Shales With Liquids-Rich Gas

By Al Pickett, Special Correspondent

As the industry continues its march into the shale gas frontier, operators are discovering huge volumes of gas reserves. In some basins, they also are finding a steady stream of natural gas liquids, which can significantly enhance the value of the production.

The question of whether gas shales contain more liquids than conventional reservoirs is still open for debate, but with U.S. gas production trending upward, NGL production is following in step. “When gas volumes increase, NGL production can be expected to increase simply because more gas is being produced,” says Ron Gist, a managing consultant with Houston-based Purvin & Gertz.

The U.S. Energy Information Administration reports that proved dry gas reserves attributable to shale reservoirs grew by 51 percent to 32.8 trillion cubic feet in 2008, or 13 percent of total domestic proved dry gas reserves. During the same year, U.S. producers added 1.1 billion barrels of NGL reserves. As one of the world’s largest NGL producers, the United States accounts for roughly one-fifth of global supply.

“Some shale gas is rich in liquids, but some is dry. It is too early to make generalizations about gas quality or liquids content in these plays,” Gist remarks, noting that some of the newest and least developed shales also appear to be some of the most significant in terms of reserves and productivity (i.e., the Marcellus in the Northeast and the Haynesville in Louisiana and Texas, as well as the Horn River in Canada). “Gas treating, dehydrating and sulphur removal has to be done everywhere–even with dry gas–but processing may not be required, depending on the characteristics of the gas.”

In the play that started it all–the Barnett Shale in North Texas–NGLs have been integral to development economics since the beginning. And as Barnett production has grown from virtually nothing a decade ago to more than 4 billion cubic feet a day, NGL output has increased correspondingly. To handle this growth, by some estimates the equivalent of a 100 million-cubic-foot-a-day cryogenic facility has been added in the Barnett every three months over the past 10 years to treat the liquids-rich gas. On average, the plants remove 3.5 gallons of NGLs for every Mcf of Barnett gas production, according to industry reports.

“The NGL market historically has been a ‘niche’ market that sort of got pushed and shoved by refiners and natural gas markets, but it is a very important market,” Gist contends. “When you have to process the natural gas, the NGLs go straight to the bottom line. This is especially advantageous when oil prices are higher than natural gas (NGLs track oil prices). Over the past several months, NGLs have been very profitable, with gas prices weaker on a Btu-equivalent basis than crude oil.”

Liquids recovery uses a cryogenic low-temperature distillation process involving gas expansion through a turbo-expander or lean oil absorption process, followed by distillation in a fractionation column, Gist explains. The recovered NGL stream is subjected to a fractionation train consisting of “de-ethanizer” (the overhead product is ethane), “depropanizer” (the overhead product is propane) and “debutanizer” (the overhead product is butanes) distillation towers.

Adding Value

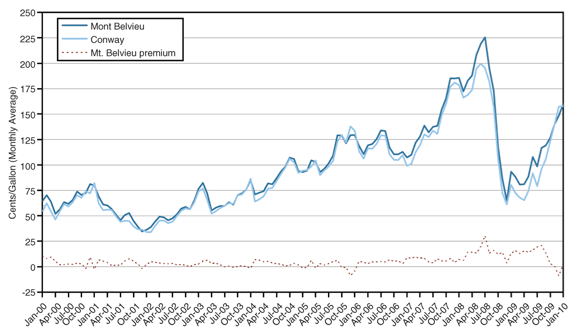

A few years ago, historically high natural gas prices left little room for profits in liquids recovery, but that situation has changed with oil prices hovering at $70-$80 a barrel and natural gas in the $5 an Mcf range. However, the products derived from NGLs are subject to just as much volatility as oil or gas. Overall, NGL product spot prices have trended on a distinct upward path since last summer, but propane spot prices at Mont Belvieu, Tx., have experienced nearly 400 percent variability since the third quarter of 2008, bouncing between lows near $0.50 a gallon and highs around $2.00 a gallon.

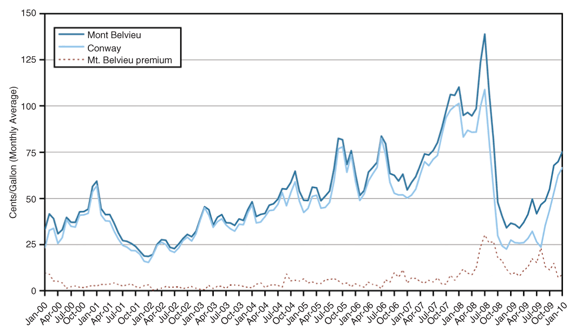

Normal butane and ethane spot prices have tracked within a similar range, with normal butane trading between $0.60 and $2.25 a gallon since summer 2008 and ethane prices posting a difference of more than $1.00 a gallon between the low and high points during the same period (Figures 1A and 1B).

Figure 1a

Spot Market NGL Price (Normal Butane)

Courtesy: R.W. Beck, an SAIC company

Source: Platt’s Oilgram News

Figure 1b

Spot Market NGL Price (Ethane)

Courtesy: R.W. Beck, an SAIC company

Source: Platt’s Oilgram News

For Oklahoma City-based Devon Energy Corporation–the top producer of Barnett Shale gas and the operator of the largest processing facility in the play (the Bridgeport plant with 620 MMcf/d capacity)–liquids recovery is a key component in the company’s business strategy.

“NGLs have the potential to add 10-15 percent to the rate of return on Barnett wells, based on the content of the liquids,” contends Jon Warzel, Devon Energy’s vice president of planning and evaluation for marketing and midstream. “NGLs are very substantial to our bottom line.”

In addition to the Bridgeport plant on the northern side of the Barnett play in Wise County, Tx., Devon owns and operates a plant in western Johnson County in the southern part of the core area. The NGLs recovered from both plants are shipped through dedicated pipelines to the Mont Belvieu hub east of Houston.

Warzel points out there are numerous variables other than oil and gas commodity prices that impact the economics of NGL recovery, including the volumes and quality of the liquid as well as the dry gas stream, petrochemical demand, the location of the production and processing sites in relation to prospective markets, etc. “All of these factors play a role in NGL economics, and all of them can be important in deciding whether it makes sense for a company to process its own gas to recover NGLs or use third-party midstream services,” he says.

Todd Morgan, vice president for crude oil and NGL marketing for Devon, adds that the NGL extraction business is made up of “a blend of processing plants owned by producers and third-party midstream companies. Deciding whether to process your own gas or use a third party depends on how active a company’s integrated midstream position is and how much critical mass it has in an area,” he remarks.

Economic conditions and weather also can have major impacts on NGL prices, according to Gist. Propane provides a case in point. “The United States often exports propane into Latin and South America,” he explains. “This year, U.S. exports of propane were up, and then we got hit with one of the coldest, wettest winters in years. As a result, propane supplies have grown tight.”

The petrochemicals market is also a key factor in NGL pricing, Gist adds. “Demand for NGLs to produce petrochemicals and plastics is an important part of the consumption picture,” he relates. “NGLs used in ethylene plants have been relatively cheap over the years, so the United States has remained an attractive place to produce petrochemicals, even though there is huge capacity in the Middle East.”

Good Margins

All things considered, the NGL market is “doing quite well, from producers to retailers to ethylene plants,” Gist holds. “It is a fairly dynamic market, and a very viable market with all the new gas from the unconventional plays across the country. Even in shale plays with drier gas, there is still a need for new treating and processing plants and pipelines, which has a lot of people scrambling.”

The industry added 1.1 billion barrels of natural gas liquids reserves in 2008, according to the U.S. Energy Information Administration. For operators such as Devon Energy with large acreage positions and midstream facilities in the liquids-rich Barnett Shale, NGLs can add incremental additional value to operating economics.

Warzel agrees that conditions have been good for the market, especially for ethane and propane. “Propane sales have been high because of the cold winter,” he says. “That pushed propane prices up, and along with them, brought up prices for ethane, which is used as petrochemical feedstock and in manufacturing plastics. Propane prices will drop when spring arrives, but processing margins have been good.”

In the past, Gist says, many producers had contracts that allowed the gas processor to keep the recovered NGLs. However, he notes that most producers have since switched to fee-based contracts, in which they pay a per-unit fee to have their gas processed and keep both the liquids and the gas.

“The gas producer is the one making the most from the gas and the NGLs,” he states. “The gas processor is often a service provider. Ten years ago, people got burned when gas prices skyrocketed, so they began switching their contracts.”

Gist adds that gas conditioning companies that charge a fee for treating gas to pipeline specifications also are doing fairly well because that business “does not have the same volatility as liquids extraction.”

Warzel says Devon maintains some agreements with third-party companies to remove contaminants from its gas, but uses Devon’s midstream division to process and treat the majority of the company’s production. He notes that Devon maintains large acreage positions in nearly all of the nation’s shale plays, giving it the operational scale to profitably process its own gas. “If a producing company has only a small acreage position, it is probably not going to be economical to put capital into building a processing facility to handle its gas,” he adds.

Liquids Variability

With annual U.S. natural gas production marking a fourth consecutive year-over-year increase in 2009, thanks to unconventional gas plays, what impact might shale gas have on NGL supply and pricing?

“Shale gas may actually tend to be drier than conventional gas, but the problem is, no one knows yet how much liquids or what quality of gas will be produced in some of these plays,” Gist responds. “The Barnett has had a lot of holes drilled to get a handle on it, but plays such as the Marcellus Shale have not been explored enough to get a feel for gas quality. I expect to see a lot of variability even within plays. For example, the gas on the east side of the Barnett Shale is dry, but 100 miles to the west, there are a lot of liquids.”

With 660,000 net acres in the Barnett, Devon is well aware of the variability in liquids content and quality across the play, and even within relatively small areas, Warzel confirms. “Every county within the core area has rich and lean pockets,” he states.

And because every shale is a little different, while NGL recovery is a key aspect in the success of the Barnett Shale, other shale plays can produce little to no liquid in the gas stream, Warzel points out.

“For example, the Woodford Shale in Oklahoma also has pockets of both rich and lean gas, similar to the Barnett, while the Fayetteville Shale in Arkansas produces very dry gas. That resource rock has different characteristics than the Barnett,” he states. “The Horn River in Canada has some liquids content. Although it is still early in the Haynesville Shale play, so far Haynesville gas has required treating, as opposed to processing, although there is a lot of acreage still to be explored.”

On the rich end of the spectrum, Warzel points to the emerging Eagle Ford Shale in South Texas as a gas play with extremely rich pockets. “Some new processing and pipeline infrastructure will have to be built in the Eagle Ford, but it has a relatively close market in the petrochemical facilities along the Gulf Coast to take the NGLs,” he states.

From the Barnett to the Eagle Ford, the development of unconventional resource plays has spurred dramatic changes in midstream infrastructure in basins across the nation, Warzel goes on. “A considerable amount of new capacity has been added in pipelines, and fractionation and processing facilities,” he relates. “In many cases, these infrastructure additions are in parts of the country that traditionally have not had natural gas production.”

Citing reports of about 1 Bcf/d in gas processing capacity scheduled to be added in the United States by 2011, Warzel says, “As rigs have moved into new play areas, companies have had to put in treating, processing and pipeline capacity to handle the gas. Initial production rates are so high in these plays that it takes a lot of coordination with midstream assets to handle the flow rates as new wells are hooked up.”

Natural gas liquids always have been integral to Barnett Shale development economics, and liquids production has increased correspondingly as Barnett gas volumes have grown. Here, a distillation tower is installed as part of a fractionation train at a Devon Energy cryogenic facility in North Texas.

Devon’s Morgan notes that a couple years ago, the nation’s pipeline grid was running full and output from a number of regions was constrained. Now, thanks to the capacity additions, the bottleneck has moved from the pipeline to fractionation capacity. “Most of the nation’s fractionation and NGL storage capacity is concentrated at Mont Belvieu, Tx., and Conway, Ks. Both these hubs handle the majority of liquids,” he remarks.

Marcellus And Markets

The Marcellus is a gas shale giant that covers some 31 million acres and holds up to 500 trillion cubic feet of in-place gas reserves, according to industry estimates. Chuck Wilkinson, president of Stonehenge Energy Resources LP, says his company has entered into a joint venture with Rex Energy Corporation to construct a cryogenic processing plant and gathering system in Butler County, Pa., to handle liquids-rich Marcellus gas, but he adds that both rich and dry gas areas likely exist within the play.

“It is sweet gas in Butler County, and the plant is designed for a fairly simple process: dehydrate and compress the gas, and provide cryogenic processing,” Wilkinson details. “We will see how the drilling goes. So far the wells are very good, and if they continue to come in as we hope, the plant’s 40 MMcf/d capacity should fill pretty quickly.”

The midstream JV operates as Keystone Midstream Services LLC (owned 40 percent by Rex Energy and 60 percent by Stonehenge), and will initially invest as much as $25 million to build the gathering and processing assets. “The cryogenic plant is expected to be completed before October 2010,” Wilkinson updates.

As more wells are drilled in the area to ramp up Marcellus production and plant throughput, Wilkinson says there are still questions about what Keystone Midstream will do with the recovered NGLs. “Who we will work with and how we will take the NGLs away are yet to be determined,” he relates. “We are working on figuring out solutions for NGL take-away.”

The problem, according to Wilkinson, is that there are no fractionation facilities near the plant and no pipelines available to transport the NGLs. Moreover, he says, there are very few petrochemical plants in the Northeast. “Since there is no NGL pipeline or local markets for all the recovered liquids, we will probably have to take the NGLs out by truck and rail, with several options for final destination,” he speculates.

The additional transportation costs associated with truck and rail shipping will impact NGL recovery economics, Wilkinson says. “It will cost more than people are used to paying in other areas of the country, but the economics can still be very positive,” he insists. “Transporting NGLs is not nearly as big an issue in the Marcellus as having pipeline access to take away the natural gas. There are any number of options available for moving NGLs by truck and rail.”

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.