Winter Fundamentals Indicate Upward Pressure On Natural Gas Prices

By David Attwood

WASHINGTON–The Natural Gas Supply Association’s Winter Outlook predicts that both natural gas demand and production will expand this winter, thanks to the recovering U.S. economy, a strong global commodity market that saw record prices in Europe and Asia during the fall, and higher wellhead prices stimulating increased domestic production.

While the long-range weather forecast calls for similar temperatures to last winter, NGSA’s forecast expects the combination of strengthening economic drivers, growing consumption of natural gas at home and around the globe this winter, and decreased storage inventory to place upward pressure on Henry Hub natural gas prices compared with last winter’s average of $3.09 an MMBtu. Responding to the stronger market fundamentals and price signals, resurgent production should keep the U.S. market sufficiently supplied throughout the heating season, according to NGSA.

NGSA’s annual analysis for the November–March heating season examines publicly reported data related to five key areas: economic indicators, weather, demand, natural gas production and storage. Although each of these potential pressure points is identified separately, all of them are interrelated. Any significant deviation of a single pressure point is likely to affect the other assumptions in the equation. The analysis provides an indication of whether market pressures on natural gas prices will be upward, downward or neutral compared with the previous winter.

Improved Fundamentals

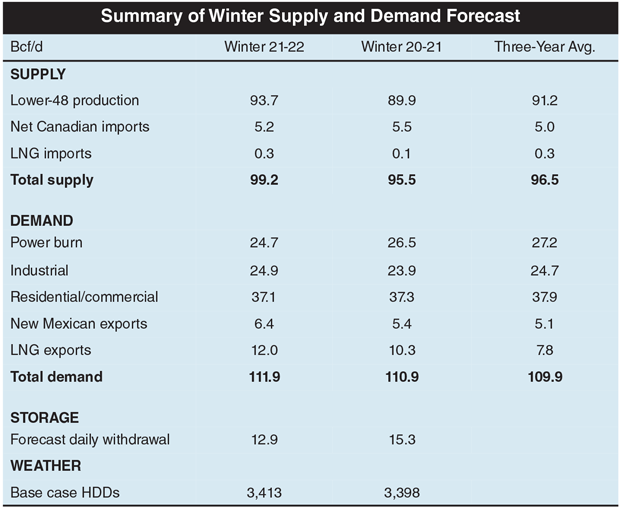

This year’s Winter Outlook forecasts upward price pressure from generally improved economic activity and from domestic storage inventories that are moderately below historic averages. Price pressures from the wintertime weather forecast and overall demand are neutral. The only downward pressure point is supply, with U.S. gas production expected to increase over the winter months, particularly in nonassociated (dry) gas shale plays (Table 1).

TABLE 1

NGSA has issued market outlooks for every winter heating season since 2001-02. The U.S. and global gas markets have evolved considerably over that period. Over the past 10 years, domestic gas production has increased by 40%, U.S. consumption has grown by 22%, and total U.S. natural gas exports are up more than three-fold, thanks to liquefied natural gas exports.

The U.S. natural gas market became significantly tighter last summer. Improved fundamentals coupled with slow production growth, strong spring and summer demand–particularly for LNG–and escalated supply concerns during the hurricane season sent Henry Hub prices to their highest late-summer levels in a decade. While prices softened somewhat as the heating season got underway in November, NGSA’s Outlook notes that they remain considerably higher this year than at the start of last winter.

Outside of the country, natural gas prices in Europe and Asia hit all-time highs in late summer and early autumn as those markets attempted to secure adequate supplies to replenish drawn-down storage inventories. A healthy rebound in post-pandemic lockdown consumption and unplanned production outages across major supply countries earlier this year slowed the refill of global gas storage last spring and summer, creating the storage imbalance as the heating season approached.

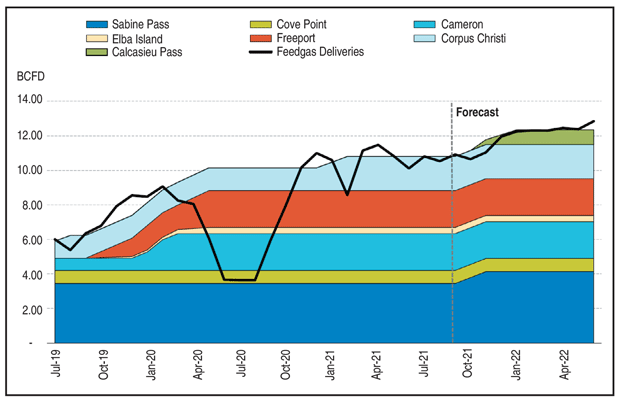

The NGSA Outlook reports that the demand pull from European and Asian markets has kept U.S. LNG exports at record levels, and coincides with new Gulf Coast liquefication capacity entering service. Expanded U.S. LNG exporting capacity and improved Mexican downstream pipeline utilization are expected to continue to result in increased total export volumes, according to the NGSA report. The U.S. Energy Information Administration forecasts that combined exports of LNG and natural gas by pipeline will average 18.3 Bcf/d in 2021 and 19.3 Bcf/d in 2022. Our modeling indicates that LNG exports will reach 12 Bcf/d in January and be sustained at the level through the spring (Figure 1).

FIGURE 1

U.S. LNG Export Capacity and Feed Gas Deliveries

NGSA’s 21st annual Winter Outlook forecasts production to provide a steady response to increased demand for domestic natural gas and LNG/pipeline exports this winter. Natural gas offers the opportunity to secure a cleaner energy future that is affordable, accessible and can help grow local economies, all while helping to reduce global emissions.

Demand Drivers

The analysis projects that total demand will reach 111.9 billion cubic feet a day this winter, slightly higher than last winter’s 110.9 Bcf/d. Domestic demand is forecasted to average 86.5 Bcf/d from the electric, industrial and residential/commercial sectors combined this winter. This represents a net decrease of 1.4 Bcf/d compared with last winter, with electric generation accounting for the reduced consumption, offset partially by the ongoing recovery in industrial demand.

Natural gas power burn is projected to decrease by 2 Bcf/d during the upcoming winter because of less temporary “economic” fuel switching to gas-fired electricity given higher anticipated natural gas prices. However, continued growth in new “structural” natural gas-fired electricity is expected with the addition of 10 gigawatts of new gas-fired capacity in 2021-2022 due to lower-emissions goals.

In contrast, the NGSA Winter Outlook projects that gas demand in the industrial market will grow 1 Bcf/d primarily because of strengthening industrial activity and improved utilization rates of facilities this winter. New-builds and capacity expansions in the gas-intensive petrochemical and fertilizer industries continue to contribute to industrial demand. Twenty-two major gas-intensive projects are planned from 2021 to 2024, collectively consuming an estimated average 1 Bcf/d of natural gas by 2024.

Demand in the residential/commercial sector is forecasted by NGSA to remain the same as last winter based on the National Oceanic & Atmospheric Administration’s forecast for a weather pattern that is quite similar (1% colder) to last winter. Using NOAA’s winter weather forecast as the base case, the end-of-March 2022 storage level is forecast at 1.69 trillion cubic feet, approaching the average of the three-year range. Projected winter 2021-22 withdrawal averages 12.9 Bcf/d, which is 2.5 Bcf/d lower than last year.

However, as was dramatically demonstrated by the massive and lingering Arctic weather event last February, weather remains the single biggest wildcard in predicting future demand among residential/commercial users. Consequently, in addition to the base case, the NGSA analyses also includes a cold-winter scenario modeled after winter 2013-14 and a warm winter scenario similar to 2015-16. According to the modeled results, residential and commercial gas demand could swing 6 Bcf/d in either direction depending on the weather. The weather sensitivity analysis shows that the end-of-March storage levels can drop well below the three-year average under a cold-winter scenario.

Looking at exports, LNG volumes are forecast to grow by +16% winter over winter while pipeline exports are expected to grow +18%, driving both to new records and representing a combined increase of 2.7 Bcf/d in U.S. exports compared with last winter. With robust demand expected to keep LNG prices at or above last winter’s level throughout the 2021-22 winter, the widening arbitrage sends a signal to U.S. LNG liquefaction terminals to operate at maximum utilization.

The completion of LNG and Mexican pipeline projects will continue to drive structural export growth, NGSA predicts. Sabine Pass Train 6 (0.65 Bcf/d) and Calcasieu Pass LNG Train 1-6 (0.43 Bcf/d) are scheduled to receive feed gas by the end of 2021. Pipeline deliveries to Mexico will also gain support from partial completion of the 0.89-Bcf/d Tula Villa de Reyes pipeline, which could improve the utilization of the main Wahalajara system.

Supply Side

The key supply factors this winter can be summarized as rebounding production and lower storage volumes. In total, natural gas supply (production, storage, and Canadian pipeline and LNG imports) is projected to average 99.2 Bcf/d this winter according to the Winter Outlook. The NGSA Outlook also projects U.S. production of natural gas to be 4% (3.7 Bcf/d) higher than last winter, reflecting the completion of large numbers of previously drilled but uncompleted wells and a growing rig count, with nonassociated gas contributing significantly to production.

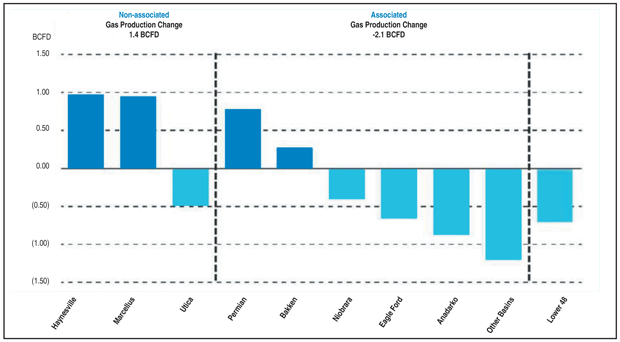

A gradual production recovery during the winter months is expected by NGSA to offset the year-over-year increase in demand. Looking at production by basin through August 2021 compared with full-year 2020, associated gas was down 2.1 Bcf/d while nonassociated output was up 1.4 Bcf/d for a net production capacity reduction of 0.7 Bcf/d. Production growth occurred in the Haynesville, Marcellus, Permian and Williston basins (Figure 2). For this winter at least, NGSA forecasts nonassociated gas growth to continue to outpace associated gas.

FIGURE 2

Production Growth by Basin (Jan-Aug 2021 versus 2020)

Despite a steady, but cautious response from producers as natural gas prices strengthened over the summer months, sustained stronger prices will likely translate into increased investment in new development projects, especially for independent gas-centric producers. The Winter Outlook forecasts the production response to higher market prices for both natural gas and crude oil to result in a 4% winter-over-winter gain in total natural gas production (associated and nonassociated).

The higher production volumes will offset reduced start-of-winter storage inventories, with U.S. storage entering the heating season in the first week of November at 3.6 Tcf, according to NGSA, putting it at 3% below the five-year average and 8% below the 4.0 Bcf that was in storage at the start of winter 2020-21.

Factoring in all five potential pressure points–economic, weather, demand, production and storage–NGSA’s annual analysis points toward upward pressure on natural gas prices this winter. But with a 40% increase in production since 2013, the shale revolution has ushered in a remarkable era, with ongoing improvements and efficiencies keeping supply flowing.

The shale revolution has benefited customers with natural gas prices that are significantly lower than other countries, and enabled reductions in carbon emissions to a 15-year low. Natural gas producers are working to do even more to support a low-emissions energy future that is affordable for all.

Editor’s Note: The preceding article was adapted from the Natural Gas Supply Association’s 21st annual Winter Outlook report, which was developed using research from Energy Ventures Analysis Inc., the U.S. Energy Information Administration, Moody’s Analytics, U.S. Bureau of Labor Statistics, and the University of Michigan. NGSA does not project wholesale or retail market prices.

DAVID ATTWOOD is chairman of the Natural Gas Supply Association and vice president of the Americas, global gas optimization and trading, at ExxonMobil. He is also a member of the Natural Gas Markets Committee at the American Petroleum Institute. Attwood began his career at ExxonMobil in 2001 as a gas marketing analyst in Australia, and subsequently served in such roles as U.S. gas marketing manager, marketing manager for U.S. equity crude sales, and director of gas marketing for XTO Energy. He holds an M.S. in physics from the University of Birmingham and an executive MBA from London Business School.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.