Natural Gas Vehicles

Fueling Capacity Key To NGV Growth

Norman Herrera

OKLAHOMA CITY– The benefits of NGVs are undeniable, positioning natural gas for substantial growth in the transportation sector, especially for medium- and heavy-duty vehicles, which account for almost one-quarter of the fuel consumed each year in the United States.

Compressed natural gas and liquid natural gas each have qualities that make it suited for specific applications. CNG, which is compressed to 3,600 psi utilizing America’s vast underground gas pipeline network, often is selected for short-haul and return-to-base applications, making it the most common natural gas transportation fuel. For over-the-road and high-mileage applications–as well as many high-horsepower, off-road applications–LNG is preferred because of its greater energy density and reduced space requirements (600 times more energy-dense in liquid form than as a gas).

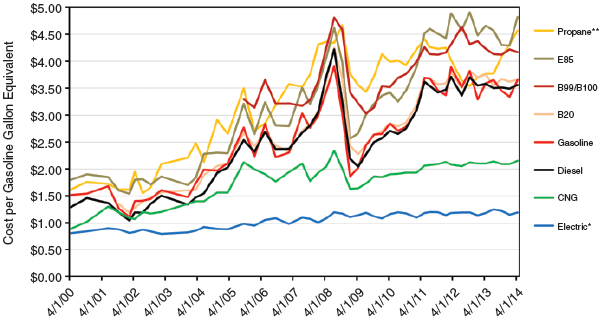

FIGURE 1

Average U.S. Retail Fuel Prices

*Electricity prices are reduced by a factor of 3.4 because electric motors are approximately 3.4 times as efficient as internal combustion engines

**Propane prices reflect the weighted average of “primary” and “secondary” stations

Natural gas-fired engines run much cleaner than equivalent-horsepower gasoline or diesel engines, but the primary appeal for both commercial fleet owners and individual consumers is the savings in fuel costs. As shown in Figure 1, the average U.S. retail price for CNG consistently averages $1.50 less than gasoline or diesel on a gasoline gallon equivalent (GGE) basis.

With the need for specialized components, the purchase price of an NGV is higher than a comparable vehicle equipped with a gasoline or diesel engine, but the lower fuel costs result in dramatic savings, depending on fuel efficiency and the number of miles driven. Heavy-duty, high-mileage fleets can realize payback on an NGV purchase within only 18-24 months.

Across the full spectrum of the NGV market–from 18 wheelers to four-door sedans–the estimated payback tends to average between 24 and 60 months, depending on miles driven and vehicle type. As engine and fuel tank technology development continues, economies of scale will continue to develop, ensuring initial vehicle costs will be lowered while further enhancing fuel efficiency to reduce the payback period.

Cleanest-Burning Fuel

As the cleanest-burning alternative fuel available, natural gas is characterized by lower greenhouse gas emissions than gasoline or diesel. In fact, the U.S. Environmental Protection Agency has acknowledged the 110-horespower, 1.8-liter i-VTEC® engine in the Honda Civic® Natural Gas as the world’s cleanest commercially available, internal-combustion engine. The CNG-powered car also meets the California Air Resources Board’s advanced technology-partial zero emission vehicle standard. According to Honda, the four-cylinder Civic Natural Gas with automatic transmission averages 38 miles per gallon on the highway, and takes less than five minutes to refuel.

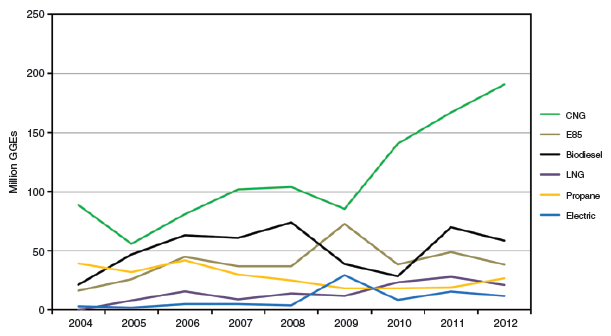

FIGURE 2

Petroleum Savings by Alternative Fuel Type

According to data from NGVAmerica, the use of NGVs resulted in a petroleum savings of 400 million gallons in 2013. Figure 2 shows the petroleum savings by alternative fuel type as compiled by Clean Cities, a national network of nearly 100 coalitions of public and private stakeholders. CNG results in more petroleum savings than any other alternative fuel type, with the increase from 2009 to 2012 being particularly striking.

In addition to reduced engine exhaust emissions and fuel costs, NGVs produce little or no evaporative and fueling emissions. Moreover, natural gas does not need any additional components or fuel additives to meet EPA requirements, thereby saving associated expenses and liabilities.

Not only do NGVs help public and private fleet operators meet their emission targets as well as internal or external green initiatives, but given the environmental advantages of natural gas, fleet operators ultimately may gain a competitive advantage in maintaining or winning contracts by committing to NGVs.

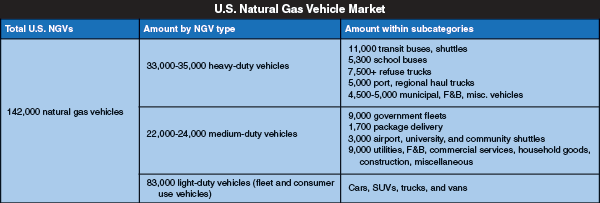

The current inventory of NGVs on U.S. roads is about 142,000, up from 130,000 in 2012. Table 1 shows a market breakdown for heavy-, medium- and light-duty vehicles. Even though light-duty vehicles are the largest category at 83,000, it is heavy-duty vehicles (33,000-35,000), with their high-mileage applications, that tend to drive consumption.

TABLE 1

Source: NGV America

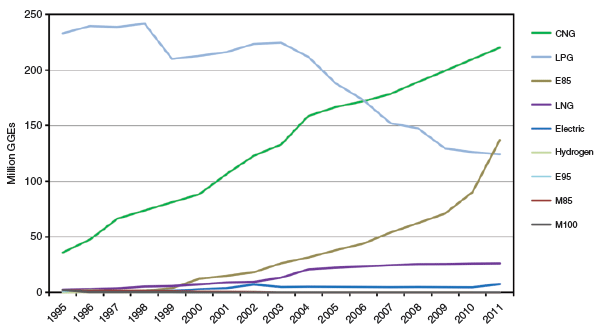

In large part as a result of CNG demand for heavy-duty vehicles, natural gas is the fastest-growing fuel type in the domestic transportation sector. Figure 3 illustrates the steady rise in CNG consumption over the past two decades. With the exception of 85 percent ethanol, the use of other alternative fuels is characterized by modest growth or decline.

Other statistics within the medium- and heavy-duty categories confirm the growth of NGVs. The American Public Transit Association reports that one-fifth of all U.S. transit buses were running on natural gas in 2012, making them the largest NGV sector. The third largest NGV sector was airport fleets. More than 35 U.S. airports either have NGVs in their own fleets or encourage their use in private fleets.

FIGURE 3

Estimated U.S. Consumption by Fuel Type

Waste collection and transfer vehicles represent the fastest-growing NGV sector, and demonstrate the success of a commercial application across the country, with almost half of all trash trucks purchased in 2012 running on natural gas.

Room To Grow

Even with NGV vehicle counts ticking upward, there is plenty of room to grow. NGV demand accounts for only a fraction of total U.S. natural gas demand. For perspective, marketed domestic natural gas production hit a record 72.7 billion cubic feet a day in March. It would take about one-fourth of that daily total (17.0 Bcf) to supply an entire year’s worth of fuel for 8,650 long-haul trucks traveling 90,000 miles annually, or 304,000 Honda Civics averaging 15,000 miles annually.

The supply capacity clearly is in place to foster sustained NGV growth over the long term, and should provide confidence to new entrants to the marketplace that a robust supply exists.

One of the historical limiting factors to achieving growth has been simply the lack of NGV availability. There are about 50 manufacturers producing 100 models of light-, medium-, and heavy-duty vehicles and engines. To expand consumer options, manufacturers and suppliers are working continually to introduce NGV models with advanced technologies, adding more options with improved capabilities to meet the needs of all classes of drivers

Engine manufacturers have introduced new designs to maximize performance, efficiency and further reduce emissions. An important market breakthrough example is Cummins Westport 12L™, a larger-displacement engine that can run on either CNG or LNG, and is suited for a wide variety of heavy-duty applications. Other manufacturers are introducing similar next-generation natural gas engines.

Innovations also are taking place with onboard fuel tanks to improve vehicle range, enhance safety, and simplify fueling. Storage tanks are one of the most expensive components in an NGV system. For instance, 3M Corp. and Rush Enterprises are cooperatively designing and manufacturing a new series of CNG tanks and fuel systems for medium- and heavy-duty trucks, and expect to launch an advanced lightweight fuel system containing several design and material enhancements in 2015.

A joint venture between Hexagon Lincoln, a manufacturer of composite CNG tanks, and Agility Fuel Systems, which builds CNG cylinder assemblies for heavy-duty vehicles, seeks to better integrate cylinder/system designs, and is building a U.S. plant to produce both CNG cylinders and onboard vehicle fuel assemblies.

Another example of strategic partnerships is an agreement between Quantum Fuel Systems Technologies Worldwide and Ryder System whereby Ryder is purchasing CNG tank systems for its trucks directly from Quantum. Ryder is the first transportation company to use Quantum’s OEM-quality CNG systems on a national scale, and the two companies are working to improve fuel system designs, providing their customers an efficient product delivery option.

Fueling Infrastructure

The vehicle market is changing and NGVs are playing a role in that change. But the pace of change will be gradual as stakeholders deal with the associated uncertainties. Developing an NGV market often is considered a chicken-or-egg proposition in that the dilemma is figuring out which should come first: the vehicles or the fueling infrastructure.

The crux of the dilemma is that without adequate fueling infrastructure in place to support NGVs, consumers are not likely to purchase them, making investing in NGV technology development uncertain for manufacturers and suppliers. On the other hand, fueling station operators need assurance of demand to justify investing in infrastructure. That makes it crucial for all stakeholders to work together in developing a proactive ecosystem to realize the full benefits of the technology, manage risk, and give confidence to consumers interested in purchasing NGVs.

The great news is that consumer willingness to switch to NGVs was measured in a 2013 survey conducted by the National Association of Convenience Stores and Penn Schoen Berland. When consumers were asked how likely they would be to consider purchasing an NGV if vehicles and fueling stations were easily accessible, 73 percent responded that they would be somewhat likely or very likely.

Not surprisingly, the greatest growth potential is in the medium- and heavy-duty market, where the benefits are the most tangible. CNG’s market share is forecast to increase significantly over the next 10 years for medium- and heavy-duty vehicles, with more moderate growth for LNG.

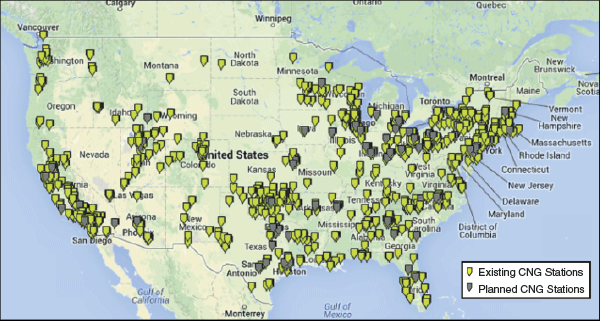

FIGURE 4

Existing and Planned CNG Fueling Stations

The challenges associated with funding, designing and constructing natural gas fueling stations to service those vehicles is being confronted head-on by increasing numbers of companies and organizations, including natural gas retailers, traditional fuel retailers, local distribution companies, oil and gas production companies, entities with large fleets, developers, and leasing companies.

As of mid-May, there were 1,383 existing and 142 planned CNG stations in the United States. Of the existing stations, 51 percent were public (up from 47 percent in 2012). Similarly, there were 93 existing and 77 planned LNG stations, with 58 percent of existing stations public (up from 39 percent in 2012). Figure 4 illustrates the locations of existing and planned public CNG stations.

Fast-fill CNG stations store natural gas in high-pressure storage vessels to ensure fast fuel transfer, similar to gasoline or diesel pumps. Time-fill CNG stations compress the gas and transfer it to onboard storage cylinders. The process is slower, but stations are less expensive to build and suitable for return-to-base fleets that can refuel while vehicles are parked overnight.

L/CNG stations dispense both LNG and CNG; the CNG is produced by compressing and flash evaporating the LNG, after which the CNG is stored in high-pressure cylinders.

Emerging technology continues to improve through the in-home refueling solution option for CNG using small systems that easily connect to a home’s natural gas supply line, compress the gas, and transfer it to the vehicle’s onboard tank while parked.

Traditionally, natural gas refueling stations are built either by fleet operators to refuel their own vehicles or by third-party companies requiring a guaranteed base load to mitigate uncertainty. However, in Sparq’s experience, the key to making CNG fueling much more accessible and convenient for potential users is to build CNG refueling capacity by retrofitting convenience stores and gasoline stations where a retail outlet already exists and customers know the location.

This approach to developing refueling capacity does not necessarily require a guaranteed base load, as with new-build public facilities. Instead, it concentrates on consumers with light- and medium-duty vehicles located in areas with identifiable markets, including regions with oil and gas production and population centers. The primary challenge normally is associated with figuring out how to manage the available space to accommodate CNG refueling.

Promoting NGV Usage

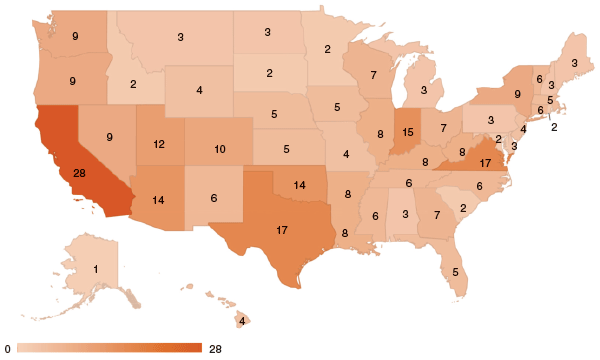

FIGURE 5

Numbers of Incentives and Laws

Related to CNG/LNG by State

There are a number of programs at both the federal and state levels that seek to promote NGV usage, including tax incentives, credits and rebates for qualified NGV purchases. The steps taken by state governments vary widely. Figure 5 provides a snapshot of the number of incentives and laws relating to CNG and LNG in each state. California has been the most active, followed by Texas, Virginia, and Indiana.

In many respects, the Texas Clean Transportation Triangle (CTT) project is a blueprint for other states to follow. It tackles the chicken-or-egg dilemma by addressing vehicle fleet conversions and refueling infrastructure in tandem, offering grants to help offset the cost of constructing refueling stations along the triangle of major highways connecting Dallas-Fort Worth, Houston and San Antonio.

According to the Texas Commission on Environmental Quality, a new-build public NGV fueling station can cost up to $3 million, depending on size, type of fuel, location, distribution lines, etc. TCEQ announced a milestone in May with the opening of San Antonio’s first public natural gas fueling station, which effectively completed the triangle when added to the network of existing stations. Two more stations are scheduled to open in the area soon. To take advantage of the growing infrastructure, a number of San Antonio-area fleet owners already have begun transitioning to natural gas.

The CTT is the fastest growing natural gas transportation corridor in the nation. Texas offers grants for creating natural gas fueling stations in the 63 CTT-eligible counties, as well as for constructing or acquiring facilities to store, compress and dispense alternative fuel in other Texas counties. In the 2014 fiscal year (ending June 30), the state received 78 applications totaling $32 million in grant requests, the vast majority of which were for proposed CNG stations.

The CTT is demonstrating the merits of natural gas on an intrastate level. On the national scale, the combination of advancing NGV engine and tank technology, expanding fueling infrastructure, and compelling economic and environmental benefits is providing a clear path for transitioning the U.S. transportation sector to capitalize on the abundance and affordability of natural gas.

In fact, there is really no other choice; natural gas represents the only clean energy option of adequate scale to facilitate meaningful growth across all market applications in the transportation sector. Fortunately, thanks to the successful development of unconventional resources, the nation is endowed with the natural gas resources to power America’s transportation sector as well as the industrial, manufacturing and electric generation sectors for generations to come.

Norman Herrera is chief executive officer of Sparq Natural Gas LLC in Oklahoma City. Before co-founding Sparq, Herrera spent six years building and directing Chesapeake Energy Corp.’s national market development team responsible for emerging technology development, infrastructure development, OEM relationships, end-user fleet relationships, policy development, and advocacy. Among his team’s strategic efforts, Herrera executed a joint development agreement with 3M for certifying and commercializing CNG pressure vessels, created and implemented the product sales strategy for General Electric CNG refueling systems, and developed and executed a partnership with Love’s Travel Stops and Corner Stores to install CNG fueling facilities. Before joining Chesapeake, Herrera served as a special assistant to Dallas Mayor Laura Miller, and as a senior budget analyst in the Dallas office of financial services. He holds a double major from Texas Tech University and a master’s with emphasis in local government management and city administration from the University of Texas at Dallas.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.