Oil Price Outlook

Price Expectations Are Driving Independents’ 2015 Drilling Plans

By Bill Campbell

It has been said that money makes the world go round. In the oil field, that translates to “price keeps rigs turning to the right.”

The question going into 2015, of course, is where crude oil prices will settle, and what effect that will have on U.S. drilling activity.

Opinions vary. In 2015 Commodities Outlook, which was released Nov. 25, J.P. Morgan forecasts a West Texas Intermediate average price of $77.25 a barrel in 2015 and $80.75 in 2016. On the lower end, the U.S. Energy Information Administration, in its December 2014 Short-Term Energy Outlook, projects the WTI spot price will average $62.75 a barrel for the year, starting at $60.33 in the first quarter and dipping to $58.33 in the second quarter before rebounding to $65.00 a barrel in the third quarter and $67.33 in the fourth quarter.

In between those two, San Francisco-based Wells Fargo predicts WTI will average $75.25 a barrel this year, according to published reports, while in its Nov. 25 Sector Comment, Moody’s Investors Service predicts WTI will average $75.00 a barrel in 2015 and $80.00 in 2016.

From yet another quarter, in a market outlook issued Dec. 9, Bank of America Merrill Lynch Global Research projects an average WTI price of $72.00 in 2015. And in a mid-December article in the Economic Times of London, Sabine Schels, an energy analyst at Bank of America, said, “We expect a pretty sharp rebound to the high $80s or even $90 in the second half of next year.”

Respondents to The American Oil & Gas Reporter’s annual Survey of Independent Operators, which was conducted between Nov. 10 and 21, indicated they were basing their 2015 drilling plans on a WTI crude oil spot price (delivered at Cushing, Ok.) of $80.00. (Editor’s Note: At press time, NYMEX crude prices for the week of Jan. 5-9 averaged $48.77.)

AOGR mails its Survey of Independent Operators to producers nationwide selected at random from the magazine’s subscription list. No attempt is made to identify survey respondents, and AOGR staff compile and analyze the data.

Big Is Better

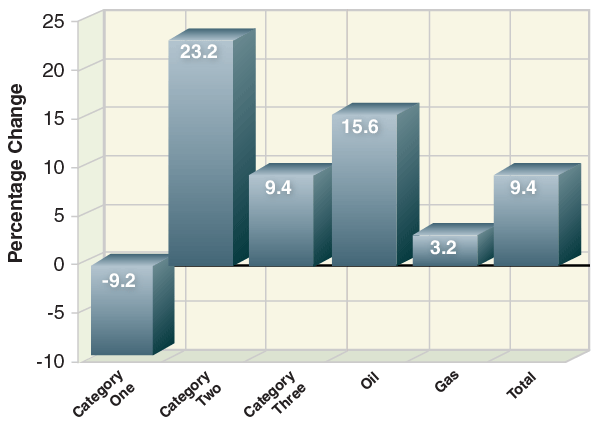

For the record, survey respondents indicated they planned to drill 9.4 percent more wells in 2015 than they did in 2014, based on a WTI spot price of $80.00 a barrel and a wellhead natural gas price of $3.86 an Mcf (see Figure 1).

FIGURE 1

Change in Operators’ Planned 2015 Drilling

Compared with 2014 Actual Drilling

Category one respondents are those that plan to drill fewer than five wells in 2015. Category two respondents plan to drill five to 12 wells this year, while category three respondents will drill more than 12 wells in 2015. Respondents included in the “oil” category targeted crude oil on more than 50 percent of their 2014 wells, while all respondents that indicated they drilled any natural gas wells in 2014 or plan to drill any in 2015 are included in the “gas” category.

However, there is a wide spread of expectations among the different categories of survey respondents. Category one respondents (those who anticipate drilling fewer than five wells this year) expect to drill 9.2 percent fewer wells in 2015 than they drilled in 2014. At the other end of the spectrum, category two respondents (those who plan to drill between five and 12 wells this year) project a 23.2 percent increase, while category three respondents (those drilling more than 12 wells in 2015) project a 9.4 percent increase.

Size does seem to make a difference in the 2015 survey. A small subset of the larger category three drillers accounted for 5.3 percent of survey respondents but 71.7 percent of 2014 wells reported by all survey respondents and 67.7 percent of 2015 wells. These very active drillers project a 3.3 percent increase in 2015 drilling, suggesting that the smallest independent operators are hurt most by falling prices and are the quickest to respond. Those in the middle, perhaps, have stronger cash flows and/or investor backing, and reflect that famous “independents’ optimism,” while the largest companies have the ability to “stay the course,” regardless of short-term price swings.

Supporting that theory is an analysis published in the Dec. 15 Oil Daily, which notes that “price pain has been most acute for smaller independent producers. A growing list of companies is slashing spending by nearly 50 percent next year.”

At the same time, the analysis continues, cuts by larger independents range between 14 and 26 percent.

An analysis posted on StreetInsider.com by Barclays analyst Thomas Driscoll suggests large independent operators are “better positioned than many investors believe them to be. Cash flows should be cushioned somewhat by continued (oil) volume growth. At $70 a barrel WTI, we estimate large-cap E&P cash flows will be down approximately 20 percent in 2015. Accounting for hedge positions among the large caps, we expect 2015 cash flows will be down about 15 percent. The impact of lower commodity prices will be somewhat, but not fully, offset by continued production growth.”

Pricing Analyses

There is another old maxim about fine print, and price projections come with caveats. In looking at its 2015 oil price predictions, EIA comments that the values of futures and options contracts suggest high uncertainty.

“WTI futures contracts for March 2015 delivery, traded during the five days ended Dec. 4, averaged $67 a barrel,” the agency details. “Implied volatility averaged 32 percent, establishing the lower and upper limits of the 95 percent confidence interval for the market’s expectations of average WTI prices in March 2015 at $51 and $89 a barrel, respectively. Last year at this time . . . implied volatility averaged 19 percent. The corresponding lower and upper limits . . . were $82 and $112 a barrel.”

J.P. Morgan acknowledges that its more optimistic price forecast of $77.25 a barrel “reflects our expectation that U.S. crude market pricing will be driven largely by international crude market developments. Inaction by the Organization of Petroleum Exporting Counties would require an adjustment by non-OPEC producers–something that likely would require prices to move materially lower than we currently envisage and take several quarters to be achieved.”

Second guessing OPEC is no easy task. At the time of OPEC’s ministerial meeting on Nov. 27 in Vienna, when WTI prices were in the range of $74 a barrel, an analysis published by BBC News noted that the national budgets of OPEC members such as Iran, Venezuela and Nigeria already were becoming hard pressed. And, “Even for those such as Saudi Arabia . . . there comes a point below which even they will start to get uncomfortable.”

The BBC published a chart, citing Deutsche Bank and the International Monetary Fund as sources, that showed the oil price needed by the various OPEC nations to balance their national budgets. It ranged from highs of $184 a barrel for Libya and $131 for Iran and Algeria, to lows of $81 a barrel for the United Arab Emirates, $78 for Kuwait and $77 for Qatar. Saudi Arabia was toward the middle at $104 a barrel.

Two weeks later, a report in Reuters quoted Venezuelan Foreign Minister Rafael Ramirez saying OPEC must act because “that is our job. We want stability in the market and predictability.”

However, the same report quoted Saudi Oil Minister Ali al-Naimi saying, “Why should we cut production?”

And a few days after that, CNNMoney quoted UAE Energy Minister Suhail Al-Mazrouei as saying, “We are not going to change our minds because the prices went to $60 or to $40.”

Finding A Cure

Going back to those old saws, “What goes up must come down.” In oil patch jargon, “The cure for low oil prices is low oil prices.”

While no one knows how far oil prices will fall or how long they will stay there before coming back up, there are a variety of opinions about the effects of various price levels.

For example, in its December Short Term Energy Outlook, EIA lowers its projection of U.S. crude oil production growth this year from 1.0 million barrels a day to 700,000 barrels a day, and comments, “Many companies will redirect investment away from marginal exploration and research drilling, and into core areas of major tight oil plays. Oil prices remain high enough to support development drilling activity in the Bakken, Eagle Ford, Niobrara and Permian Basin, which contribute the majority of U.S. oil production growth.”

Morgan Stanley, likewise, has cut its estimate of U.S. production growth this year from 1.0 MMbbl/d to 700,000 bbl/d, according to published reports, and IHS Inc., which also is predicting U.S. production will increase by 700,000 bbl/d this year, says, “Most of the potential U.S. tight oil capacity additions in 2015 (about 80 percent) have a break-even price in the range of $50 to $69 a barrel.”

On Dec. 15, when the WTI spot price at Cushing closed at $55.96, Natural Gas Intelligence’s Shale Daily quoted Wunderlich Securities analyst Irene Haas as predicting more than 500 rigs could be idled within 60 days. In the same article, Tudor, Pickering, Holt & Co. suggested “a sustained price of $60 a barrel” could result in yet another 300-rig decline.

Credit Suisse predicts a 25 percent decrease in U.S. drilling at $75 a barrel oil.

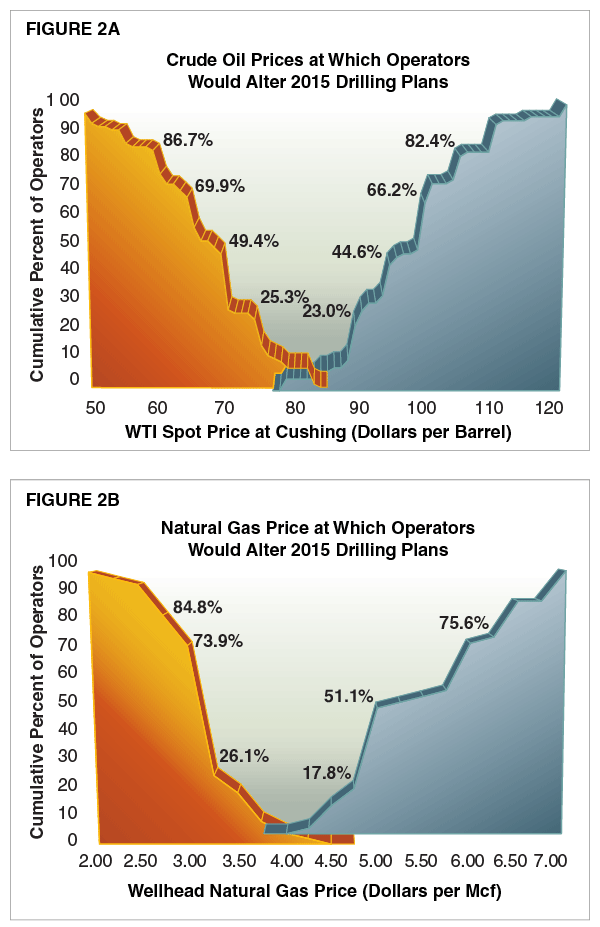

Percentages in Figures 2A and 2B represent the cumulative total of survey respondents that indicate they would have altered their 2015 drilling plans by the time the spot price for West Texas Intermediate crude oil delivered at Cushing, Ok. (Figure 2A), or the wellhead natural gas price (Figure 2B), reached the indicated amount. Prices at which drilling would decrease are plotted to the left of the graphs in downward curves; prices at which drilling would increase are plotted to the right of the graphs in upward curves.

Others, however, are more positive. Citigroup calculates break-even costs for U.S. shale oil projects “are almost all below $70 in Brent prices (about $60 WTI), sometimes much lower.” Citigroup adds that its base case projection shows, “If Brent prices stay in the $75-$85 range, with WTI about $10 lower, minimal impacts to shale are expected.”

A Wood Mackenzie analysis adds, “WTI needs to fall below $70-$65 a barrel for several quarters before there will be a significant slowdown in U.S. tight oil production growth.”

And in its BDO U.S. 2015 Energy Outlook Survey, which presents the perspectives of chief financial officers at oil and gas exploration and processing firms, BDO USA LLP reports that when asked to identify their strategies for improving profitability in 2015, 56 percent of respondents pointed to cutting costs and seeking efficiencies, compared with 27 percent that would look to new technologies, and only 9 percent who said they would reduce exploration.

If accurate, that prediction may affirm the observation by numerous analysts that enough commitments and projects are “in the pipeline” already to keep U.S. production growing for some time. Or to borrow another phrase, “Locomotives don’t stop on a dime.”

Survey Results

AOGR’s Survey of Independent Operators asks respondents what crude oil and/or natural gas price would cause them to both reduce and increase the number of wells they plan to drill in the coming year.

As seen in Figure 2A, 25.3 percent of respondents say they would decrease their planned drilling this year at a WTI spot price of $75 a barrel. That percentage grows to 49.4 at $70, to 69.9 at $65, and to 86.7 at $60.

On the upside, 23.0 percent of respondents indicate they will increase the number of wells they plan to drill this year if oil prices return to $90 a barrel. That percentage increases to 44.6 at $95, to 66.2 at $100, and 82.4 at $105.

Looking at natural gas (Figure 2B), 17.8 percent of respondents will drill more wells at $4.75 an Mcf, 51.1 percent will increase drilling at $5.25, and at $6.25 an Mcf, 75.6 percent of respondents will drill more wells.

Going the other way, 26.1 percent of survey respondents say they will drill fewer wells if natural gas prices fall to $3.25. From there, the percentage of respondents who would decrease drilling balloons to 73.9 at a gas price of $3.00 an Mcf, and to 84.8 at $2.75 an Mcf.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.