Market Outlook

EIA, IEA Increase Global Oil Demand Projections

WASHINGTON–According to the U.S Energy Information Administration, global oil consumption is rallying back and is poised to accelerate to 101.2 million barrel a day in 2022, topping pre-pandemic levels.

In its April Short-Term Energy Outlook, EIA says the world consumed 96.0 MMbbl/d of petroleum and liquid fuels in March, an increase of 4.7 MMbbl/d over March 2020. “We forecast that global consumption will average 97.7 MMbbl/d for all of 2021, which is up 5.5 MMbbl/d from 2020. We forecast that consumption will increase by 3.7 million b/d in 2022 to average 101.3 MMbbl/d.”

On the natural gas side of the ledger, the agency estimates that consumption will decline slightly this year compared to last because of significantly higher forecast prices softening demand in the electric power generation sector. On a percentage basis, EIA expects that the share of electric power generated with natural gas will average 36% in 2021 and 35% in 2022, down from 39% in 2020.

“The forecast share for natural gas declines in response to a 39% increase in the price of natural gas delivered to electricity generators, from an average of $2.39/MMBtu in 2020 to $3.31/MMBtu in 2021,” the STEO states.

However, EIA projects that gas demand will rebound through 2022 in both the residential/commercial and industrial sectors. “Rising consumption outside of the power sector results from expanding economic activity and colder temperatures in 2021 compared with 2020,” it states. “We expect U.S. natural gas consumption will average 82.1 billion cubic feet a day in 2022.”

U.S. crude oil production is forecast to average 10.9 MMbbl/d in the second quarter and then gradually increase to 11.4 MMbbl/d by the fourth quarter and 11.9 MMbbl/d in 2022. The forecast of rising U.S. oil production is the result of EIA’s expectation that West Texas Intermediate prices will remain above $55/bbl through the forecast period.

U.S. production of dry natural gas will average 91.4 Bcf/d in 2021, or about the same as the 2020 average, according to EIA. “In our forecast, dry natural gas production falls to a low point of 90.8 Bcf/d in May before steadily increasing through most of the remainder of 2021, reaching a high of 92.4 Bcf/d in November. The increased production reflects higher forecast natural gas and crude oil prices, which we expect will contribute to more associated natural gas production, especially in the Permian Basin region.”

Well Productivity

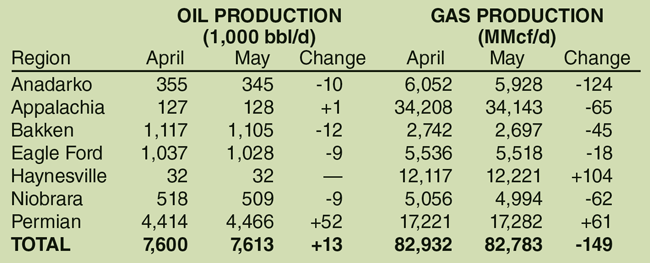

In its latest Drilling Productivity Report, EIA projects that the major shale basins will produce 7.6 MMbbl/d of oil and 82.9 Bcf/d of gas in April (Table 1). That compares with 8.7 MMbbl/d of oil and 82.9 Bcf/d of gas in April 2020. The Permian is expected to average 4.4 MMbbl/d compared with 4.6 MMbbl/d a year earlier. Oil output in the Bakken is estimated to average 1.1 MMbbl/d versus 1.4 MMbbl/d in April 2020, while the Niobrara is pegged at 518,000 this April compared with 782,000 last April.

TABLE 1

Forecast Production by Regions (U.S. Shale Plays)

However, the amount of new well production per rig is dramatically higher, which is partly an artifact of the lower drilling and completion activity levels and high-grading development acreage. According to EIA, April’s 1,125 bbl/d of new-well oil production per rig far eclipsed the 730 bbl/d rig-weighted average in the same month a year ago. By region, new-well oil production is estimated at 1,249 bbl/d per rig in Permian, 2,427 bbl/d in the Bakken, and 1,936 bbl/d in the Niobrara versus 677, 1,249 and 1,106 bbl/d per rig, respectively, in April 2020.

The increase is even more pronounced for natural gas, with average new-well gas production per rig effectively doubling from 3,420 Mcf/d in April 2020 to 6,869 Mcf/d in April 2021. Gas well productivity is led by the Marcellus (from 14,583 to 27,708 Mcf/d) and Haynesville (from 9,782 to 11,425 Mcf/d).

The numbers of drilled but uncompleted wells in inventory has fallen by 688 year over year, from 7,600 to 6,912 in March. The majority of DUCs remain concentrated in the Permian and Eagle Ford, although the numbers in both plays have declined year over year.

Robust Indicators

In line with EIA’s upward revision on global oil demand, the International Energy Agency’s April Oil Market Report increased forecast oil consumption by 230,000 bbl/d on average to “take account of better economic forecasts and robust prompt indicators.” IEA projects that oil demand will reach 96.7 MMbbl/d in 2021, a year over year increase of 5.7 MMbbl/d.

IEA points out that global refinery throughput caught up with year-earlier levels in March for the first time since 2019, rising by 1 MMbbl/d month-over-month on a strong recovery in the United States following February’s deep freeze. At 75.9 MMbbl/d, global refinery runs were nevertheless 4.4 MMbbl/d below March 2019. Crude throughput is forecast to rise by 6.8 MMbbl/d from April to August, resulting in average annual growth of 4.5 MMbbl/d.

Global crude oil and refined product inventories also continued to trend in the right direction, IEA says. OECD stocks fell for the seventh consecutive month in February, by 55.8 million barrels, or 2 MMbbl/d, led by a sharp draw in product inventories (-66.8 million barrels). At the end of February, total oil stocks stood at 2,977 million barrels, reducing the overhang versus the 2016-2020 average to 28.3 million barrels.

“A year on from what the IEA called ‘Black April,’ one of the darkest months ever for world oil markets, fundamentals look decidedly stronger. The massive overhang in global oil inventories that built up during last year’s demand shock is being worked off, vaccine campaigns are gathering pace, and the global economy appears to be on a better footing,” the report states.

Even as the outlook brightens considerably for oil demand, IEA cautions that prices could come under renewed short-term pressure with world oil supply set to ramp up and shift the market from deficit towards balance. OPEC+ agreed on April 1 to gradually ease output cuts by more than 2 MMbbl/d from May through July. However, the longer term remains bullish.

“The market changes dramatically in the latter half of this year as nearly 2 MMbbl/d of extra supply may be required to meet expected demand growth, even after factoring in the announced ramp up of OPEC+ production,” IEA relates. “Global refinery runs are forecast to rise by 6.8 MMbbl/d from April to August, just as crude oil-fired power generation rises seasonally.”

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.