New LNG Export Capacity In U.S, Mexico And Canada Has Significant Implications

By Housley Carr

HOUSTON–There is a giant wave of incremental demand for U.S. natural gas coming in the form of new liquified natural gas export capacity, and it has the potential to reshape the dynamics of the domestic gas market.

During the next five years, the U.S. Gulf Coast is poised to experience another big increase in new LNG export capacity, and this time it will be joined by new capacity coming on line in both Mexico and Canada. The more than 13 billion cubic feet a day of incremental natural gas demand from the new North American LNG projects will have significant effects on U.S. and Canadian gas producers, gas flows and—quite likely—gas prices.

There are 10 North American LNG export projects in very advanced stages of development. As they come on stream and begin liquifying gas for export, there may be a number of broad implications for gas markets. One thing is for sure: the expected ramp-up in LNG-related gas demand will be warmly welcomed by U.S. natural gas producers, who have spent more than a year contending with low wellhead prices.

LNG Export Licenses

The Biden administration’s announcement in late January of a temporary pause in approving new LNG export licenses to non-Free Trade Agreement (non-FTA) countries—or extending existing licenses, barring special circumstances—grabbed headlines and raised energy-industry hackles. Although the pause has cast a shadow over several LNG export proposals nearing final investment decisions, it has had little or no impact on the long list of projects that already have those U.S. Department of Energy export licenses in hand.

In fact, the pause may well have a positive effect on a few U.S. and Mexican projects that already have non-FTA licenses, as well as Canadian projects that do not need them, but had not yet received a final go-ahead from their developers earlier this year when the administration made the announcement.It must be noted that a number of major LNG-importing countries and regions fit into the “non-FTA” category, including the United Kingdom, the European Union, Japan, China, India, Brazil and Argentina. Moreover, it is also important to keep in mind that on July 1, a federal court judge in Louisiana ordered that the pause be “stayed in its entirety, effective immediately,” but the practical effects of that ruling remain unclear.

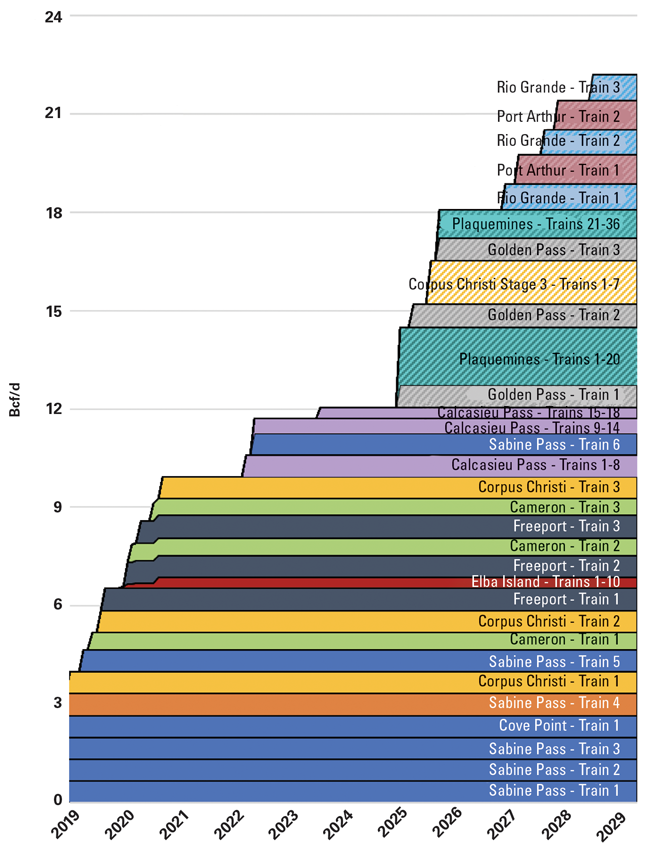

In any case, there is a long list of North American LNG projects—large, medium and small—that have reached an FID and are either under construction or about to enter that phase. Let’s start with the United States, which already has 12 Bcf/d of LNG export capacity in operation and is expected to add another 6.4 Bcf/d by early 2026 and an additional 3.9 Bcf/d between 2027 and 2029 (Figure 1). Adding these new terminals will put U.S. LNG export capacity at more than 22 Bcf/d by the end of this decade.

Five U.S. Projects

The 10.3 Bcf/d in incremental LNG export capacity slated to start operations during the next five years is tied to five post-FIDs projects, all of which are under construction. Those five projects include:

- Venture Global’s 2.6-Bcf/d Plaquemines LNG terminal;

- Cheniere Energy’s Corpus Christi Stage 3 expansion;

- The three-train, 2.4-Bcf/d Golden Pass LNG project;

- NextDecade Corp.’s three-train, 2.1-Bcf/d Rio Grande LNG facility; and

- Sempra Infrastructure and ConocoPhillips’ two-train, 1.8-Bcf/d Port Arthur LNG plant.

The Plaquemines LNG facility is located 20 miles south of New Orleans in Plaquemines Parish, La. The first of the project’s 36 modular “mini-trains” are expected to begin commissioning in the back half of this year and the entire facility is scheduled to be fully on line in 2026.

FIGURE 1

Existing and post-FID U.S. LNG Export Capacity

Corpus Christi Stage 3 has seven midscale modular trains with a combined capacity of 1.4 Bcf/d. The project is an expansion of Cheniere’s existing Corpus Christi LNG terminal in South Texas. A mid-June Cheniere presentation reported Stage 3 construction was more than 60% complete and ahead of schedule. The company has also indicated that initial LNG production is likely by the end of this year and that all seven trains should be up and running by late 2025 or early 2026.

Golden Pass is co-owned by a 70/30 joint venture of QatarEnergy and ExxonMobil. The project’s co-developers predict the commissioning of train one will begin in the first half of 2025, followed by the startup of train two in late 2025 and train three in early 2026.

However, the pace of work going forward at Golden Pass may be impacted by lead EPC contractor Zachry Group’s late-May filing for federal bankruptcy protection, a move the builder tied to “significant financial strain” from ongoing project-cost battles with QatarEnergy and ExxonMobil. Zachry said in its filing that it was exploring a “structured exit” from the project and that its construction partners on the job, Chiyoda Corp. and McDermott International, were continuing work. It remains to be seen if the matter will impact Golden Pass’s timeline.

It is worth noting that on March 2020 the DOE granted Golden Pass a 17-month extension on the project’s non-FTA export license to September 2025. Whether a further extension may be needed is yet to be determined.

Train one of NextDecade Corp. Rio Grande LNG project in Brownsville, Tx., is scheduled to come on line in mid-2027, followed by train two in early-to-mid-2028 and train three in late 2028 or early 2029.

The Sempra and ConocoPhillips-operated Port Arthur facility is also on schedule, with train one slated to start operating in the second half of 2027 and train two to follow suit in the first half of 2028. In April, a couple of months after the Biden administration announced its pause in approving non-FTA export licenses, DOE granted a 25-month extension to Port Arthur’s license, giving that project until June 2028 to come on line. In its decision, DOE noted that the project was already under construction, which it considered an extenuating circumstance that justified the extension.

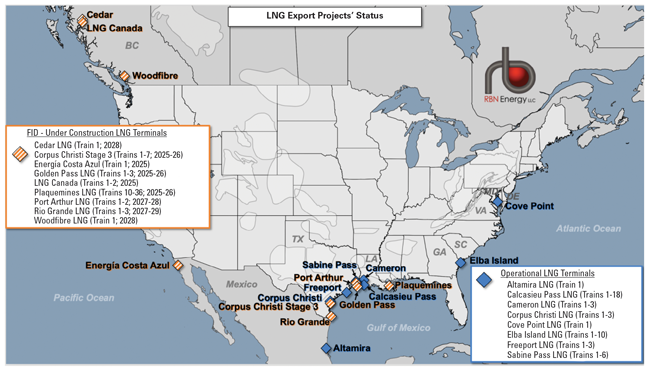

Mexican, Canadian Terminals

Looking farther south at the Mexican LNG projects in advanced stages of development, one facility actually has been finished recently while the other is nearing completion (Figure 2). Although these projects are located south of the border, they will depend on U.S. gas supplies (mostly from the Permian and Eagle Ford), so they need DOE export licenses if they plan to send LNG to non-FTA countries.

Sempra is well along in the construction of a 300 million cubic feet a day liquefaction train at its Energía Costa Azul LNG (aka ECA) in Baja California—a facility initially developed as an LNG import terminal—and expects to bring that train on line in mid-2025. ECA has a non-FTA export license. New Fortress Energy recently finished building Altamira LNG, a new, 400 MMcf/d export terminal along Mexico’s East Coast that still lacks a non-FTA export license. New Fortress has been saying for some time that its first LNG shipment is imminent—without the DOE license. Destination possibilities may include Puerto Rico (the project is exempt from the Jones Act) or a trio of nearby LNG-importing countries that have free trade agreements with the United States: the Dominican Republic, Panama and Colombia.

And then there is Canada, which has three post-FID LNG export projects. Each of the projects will export natural gas produced in British Columbia or Alberta, and therefore, do not require any U.S. licenses or other approvals. The largest and furthest along is LNG Canada, a two-train, 1.8-Bcf/d project located in Kitimat, BC. The project is being co-developed by an international consortium that includes Shell Canada (with a 40% stake), Petronas (25%), PetroChina (15%), Mitsubishi (15%) and KOGAS (5%). Both trains at LNG Canada are expected to come on line in mid-2025.

FIGURE 2

LNG Export Projects in the U.S., Mexico and Canada

Also in British Columbia, Woodfibre LNG, a 300 MMcf/d project in Squamish that is 70%-owned by Pacific Energy and 30%-owned by Enbridge, is in the very early stages of construction. The project, which is slated to direct its LNG output to BP, is expected to start operations by 2028.

The latest entrant is the 400 MMcf/d Cedar LNG facility, also in Kitimat. The project’s JV partners (Pembina Pipeline and the Haisla Nation) took FID on the floating, single-train project in late June. The project appears to have benefited from the U.S. pause in issuing export licenses. The JV predicts Cedar LNG will begin commercial operation in late 2028.

Assuming all three of these projects start operations as planned, Canada will send out 2.5 Bcf/d of LNG by 2029.

Positive Effects

The new LNG export capacity coming on line in North America during the next few years is sure to have a significant impact on gas production, gas flows and gas prices both in the United States and Canada. Given that all the incremental U.S. export capacity is located along the Gulf Coast, gas produced at crude-oil-focused wells in the Permian Basin—often selling at negative prices at the Waha Hub lately—will have new outlets, which should strengthen regional gas prices, especially considering that the Permian also will be a primary supplier to the new LNG export facilities in Mexico.

In a similar vein, demand for gas produced in Western Canada’s Montney Shale play will increase as LNG Canada, Woodfibre LNG and Cedar LNG start operations, likely resulting in a further reduction in pipeline gas exports across the border from western Canada into the U.S. market. Diminishing gas volumes coming from the north also may support stronger U.S. gas prices in light of the additional baseload demand required to support the new U.S. LNG export capacity.

There are a couple more possible implications. First, higher LNG exports may reduce the spread between U.S. gas prices and international markets such as the Title Transfer Facility, with the obvious caveat that there always will be the transport arbitrage, so U.S. prices will continue to lag behind those in international markets as a result of shipping costs.

Second, in the longer term, more U.S. LNG exports may require more production from gas-focused plays such as the Haynesville, which may necessitate higher gas prices.

As always with natural gas prices, a lot of wild cards can factor into the equation. Nevertheless, the prospect of market dynamics setting up in favor of stronger gas prices will be an obviously positive sign for producers after more than a year of sub-$3 per million Btu Henry Hub prices.

HOUSLEY CARR is an energy writer/analyst at Houston-based RBN Energy, where he authors blogs and reports on both domestic and international crude oil, natural gas, NGL, LNG and refined products markets. Before joining RBN in 2013, Carr had served for 36 years as an energy and environmental journalist for industry and trade publications. He holds a B.A. from the University of Virginia.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.